Mortgage Rates

What Is Going on with Mortgage Rates?

You may have heard mortgage rates are going to stay a bit higher for longer than originally expected. And if you’re wondering why, the answer lies in the latest economic data. Here’s a quick overview of what’s happening with mortgage rates and what experts say is ahead.

Economic Factors That Impact Mortgage Rates

When it comes to mortgage rates, things like the job market, the pace of inflation, consumer spending, geopolitical uncertainty, and more all have an impact. Another factor at play is the Federal Reserve (the Fed) and its decisions on monetary policy. And that’s what you may be hearing a lot about right now. Here’s why.

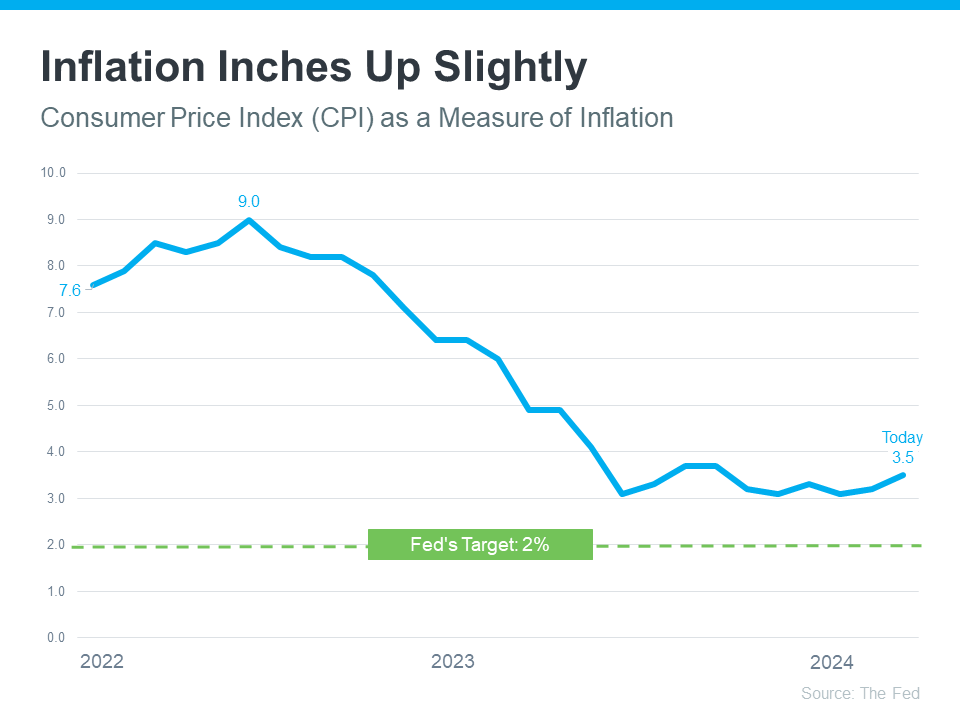

The Fed decided to start raising the Federal Funds Rate to try to slow down the economy (and inflation) in early 2022. That rate impacts how much it costs banks to borrow money from each other. It doesn’t determine mortgage rates, but mortgage rates do respond when this happens. And that’s when mortgage rates started to really climb.

And while there’s been a ton of headway seeing inflation come down since then, it still isn’t back to where the Fed wants it to be (2%). The graph below shows inflation since the spike in early 2022, and where we are now compared to their target rate:

As the graph shows, we’re much closer to their goal of 2% inflation than we were in 2022 – but we’re not there yet. It’s even inched up a hair over the last 3 months – and that’s having an impact on the Fed’s plans. As Sam Khater, Chief Economist at Freddie Mac, explains:

“Strong incoming economic and inflation data has caused the market to re-evaluate the path of monetary policy, leading to higher mortgage rates.”

Basically, long story short, inflation and its impact on the broader economy are going to be key moving forward. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“It’s the longer-term outlook for economic growth and inflation that have the greatest bearing on the level and direction of mortgage rates. Inflation, inflation, inflation — that’s really the hub on the wheel.”

When Will Mortgage Rates Come Down?

Based on current market data, experts think inflation will be more under control and we still may see the Fed lower the Federal Funds Rate this year. It’ll just be later than originally expected. As Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), said in response to the Federal Open Market Committee (FOMC) decision yesterday:

“The FOMC did not change the federal funds target at its May meeting, as incoming data regarding the strength of the economy and stubbornly high inflation have resulted in a shift in the timing of a first rate cut. We expect mortgage rates to drop later this year, but not as far or as fast as we previously had predicted.”

In the simplest sense, what this says is that mortgage rates should still come down later this year. But timing can shift as new employment and economic data come in, geopolitical uncertainty remains, and more. This is one of the reasons it’s usually not a good strategy to try to time the market. An article in Bankrate gives buyers this advice:

“ . . . trying to time the market is generally a bad idea. If buying a house is the right move for you now, don’t stress about trends or economic outlooks.”

Bottom Line

If you have questions about what’s happening in the housing market and what that means for you, connect with a trusted real estate professional.

There’s a lot of uncertainty right now and that’s leading to some dramatic headlines. And if you’re thinking about buying a home, that can make you feel a little less sure about your decision.

A recent study by CNBC asked homebuyers what they’re most worried about, and three themes kept coming up again and again:

- Mortgage rates

- The number of homes for sale

- Home prices

But a lot of what you may be hearing on those is based more on misconceptions. Not facts. So, let’s break it down and separate fact from fiction.

Misconception #1: “I’ll Just Wait, Because Mortgage Rates Are Going To Fall Dramatically”

One idea doing its rounds on social is that mortgage rates are going to drop dramatically soon. So, it’s better to wait to buy.

But is that really what’s expected?

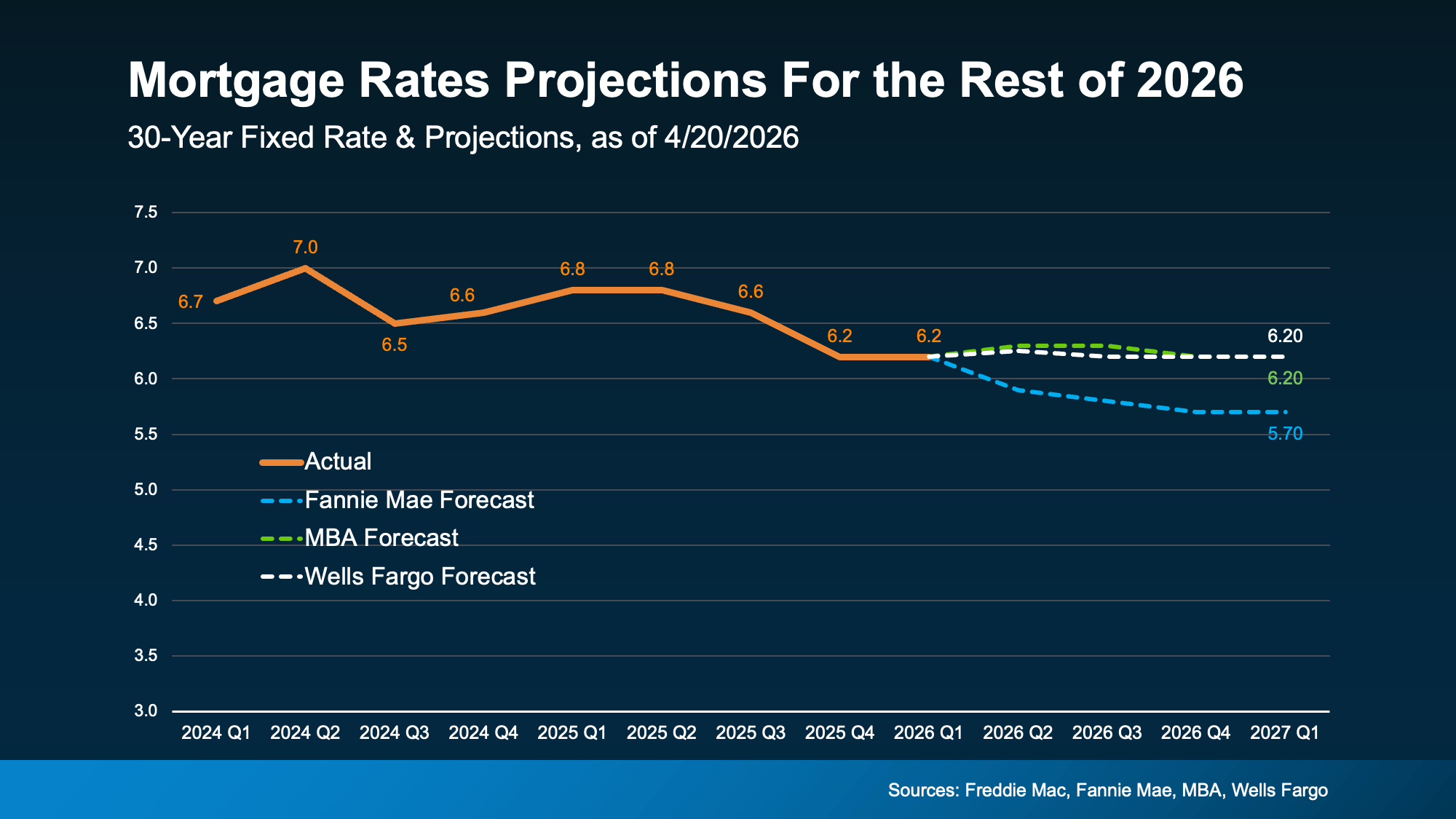

While mortgage rates have come down a bit in the last few weeks, forecasts don’t show a major drop ahead. The most likely scenario is that rates stay somewhere in the low 6% range this year.

And that’s not a big change from where rates are now (see graph below):

Of course, this depends on where inflation and the economy go from here. But, based on what we know today, waiting for a big drop in rates may not work out the way some people hope. As U.S. News explains:

Of course, this depends on where inflation and the economy go from here. But, based on what we know today, waiting for a big drop in rates may not work out the way some people hope. As U.S. News explains:

“Mortgage rates aren’t expected to change much over the next several quarters . . .”

Not to mention, even with rates where they are today, it’s already more affordable than a year ago. So, even if they don’t change much, it’s still better than it was.

Misconception #2: “There Are Too Many Homes for Sale Right Now”

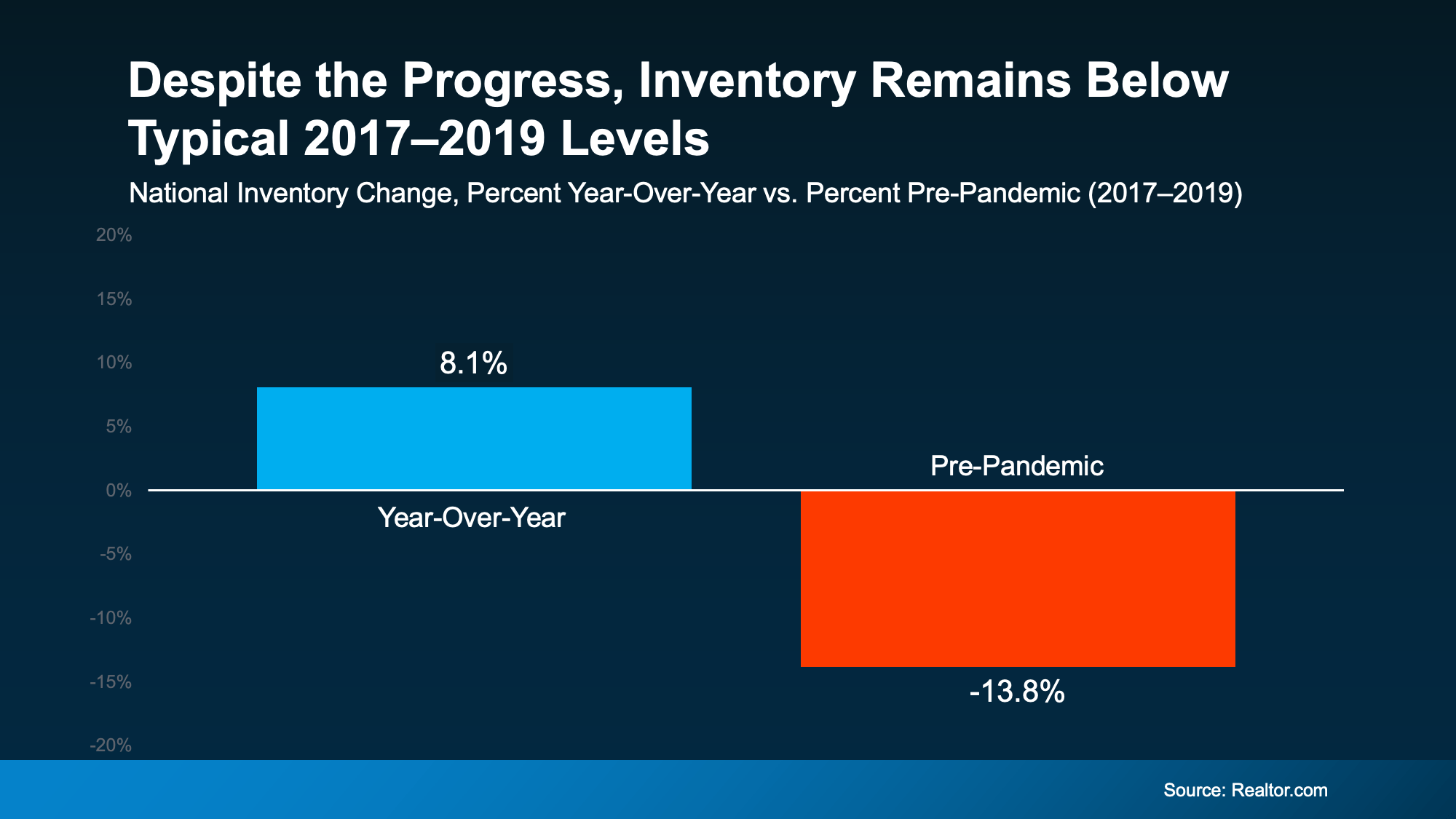

You’ve probably heard inventory is up. And nationally, it is. The number of homes for sale is 8% higher than this time last year. But that’s not a bad thing. In fact, it’s one of the reasons buyers have a bit more breathing room right now.

The problem is the headlines are making something good, sound bad. They’re focusing on how this is the most inventory we’ve had since 2019 or how many homes builders are building. And that can make it sound like the number of homes for sale is rising too far, too fast.

But that’s not what the bigger picture shows.

Data from Realtor.com proves that, even though inventory is up compared to last year, it’s still nearly 14% lower than it was during the last normal housing market (2017-2019):

While it can vary a lot based on where you live, only 9 states have more inventory than pre-pandemic today. That’s a key reason why there still aren’t enough homes for sale to trigger something like the crash back in 2008.

While it can vary a lot based on where you live, only 9 states have more inventory than pre-pandemic today. That’s a key reason why there still aren’t enough homes for sale to trigger something like the crash back in 2008.

Misconception #3: “Home Prices Are About To Crash”

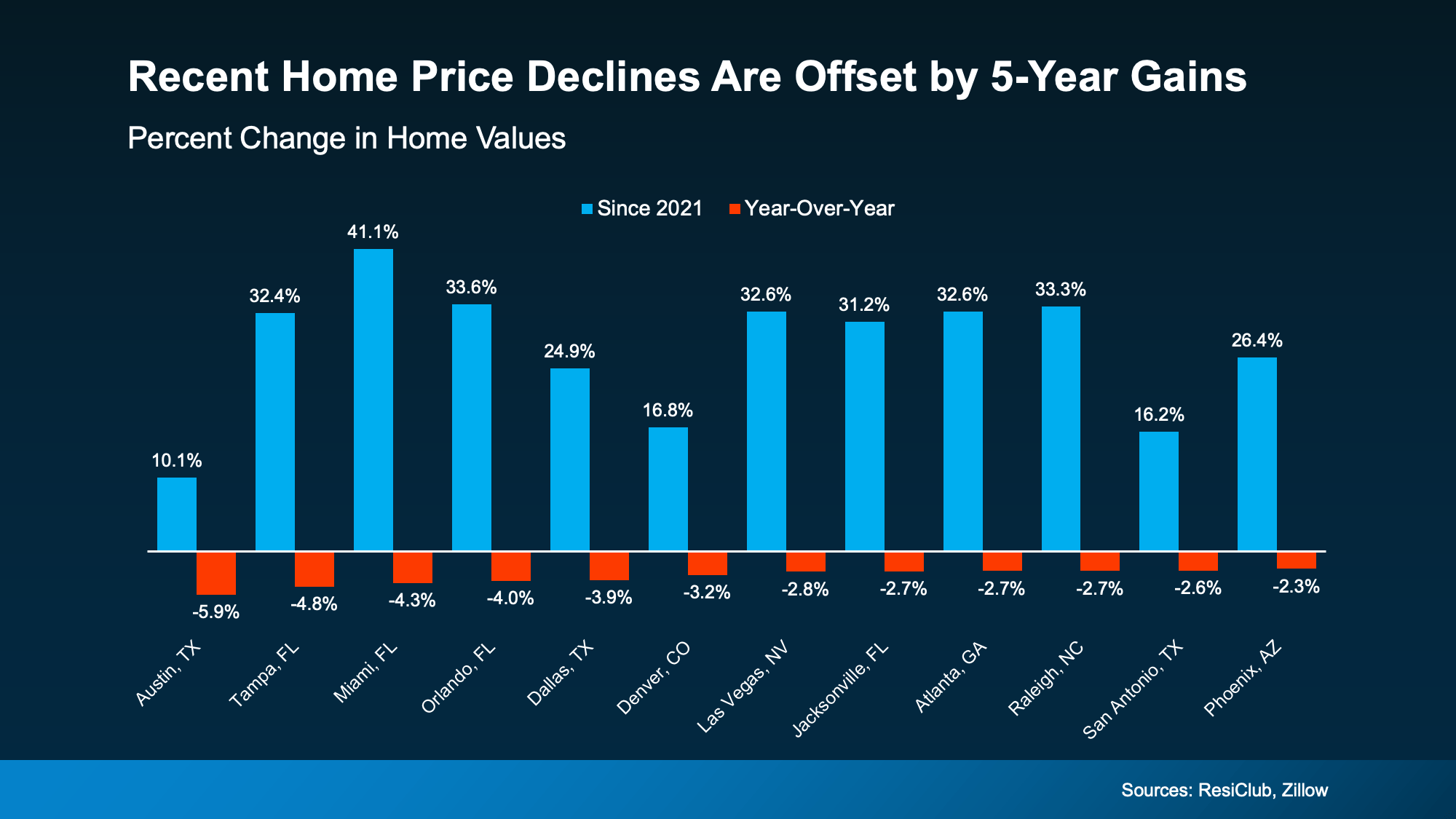

You’ve probably seen this one, too. The confusion is coming from the fact that some metros are experiencing slight price declines. And influencers are running with that and saying prices are crashing. But that’s not the reality.

Most areas are seeing prices rise, not fall. And that’s because:

- Many homeowners aren’t selling because they don’t want to give up the low mortgage rate they locked in a few years ago. And that’s keeping a lid on how much inventory can grow.

- Since inventory is still below pre-pandemic norms, there aren’t enough homes for sale to cause a price crash.

- And even in markets with more inventory, some sellers are choosing to pull their homes off the market instead of cutting prices.

And those are 3 big reasons prices aren’t headed for a crash.

And even in the markets experiencing mild declines, the drops aren’t enough to cancel out the big gains most homeowners have seen in the last 5 years (see graph below):

That’s not a crash. That’s just prices moderating after a few record-breaking years.

That’s not a crash. That’s just prices moderating after a few record-breaking years.

Bottom Line

Online posts are going to make things sound worse than they are. If you want a true, data-bound look at what’s really happening in today’s market, lean on a real estate agent.

Connect with a local agent so you have someone to separate fact from fiction today.

If you’ve been looking for a home lately, you’ve probably felt how tough affordability still is. And that’s exactly why more buyers are opting for adjustable-rate mortgages, or ARMs.

Here’s what you need to understand about how they work, and whether they make sense for you.

What Is an Adjustable-Rate Mortgage?

Since a lot of people aren’t familiar with this type of loan, let’s start with a definition. This is how Business Insider explains the main difference between a fixed-rate mortgage and an adjustable-rate mortgage:

“With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You’ll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they’ve gone down, your payment will decrease.”

Basically, one doesn’t change much over the life of your loan.

And one could change… either by a little, or a lot.

Of course, things like taxes or homeowner’s insurance can still have an impact on a fixed-rate loan, but the baseline of your mortgage payment is fairly steady. But the big difference is that with an ARM, your monthly payment could change over time.

Why Adjustable-Rate Mortgages Are Getting More Attention

So, why do some buyers choose this option? It’s simple. It’s because of the upfront savings. Business Insider explains it like this:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan.”

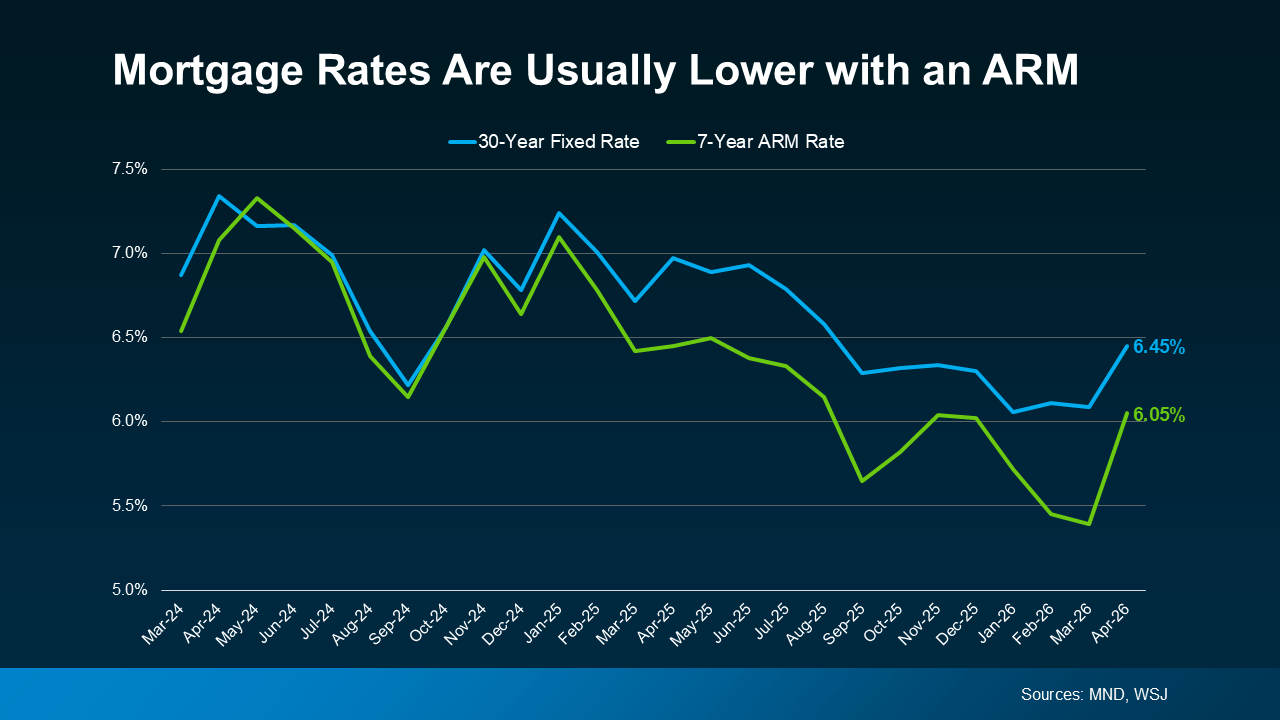

And right now, according to Mortgage News Daily and the Wall Street Journal, the upfront rate on an ARM is lower than a 30-year fixed mortgage (see graph below):

If you’re wondering how that shakes out in real dollars and cents, here’s what Redfin says. According to their research, the typical buyer could save about $150 per month by taking out an ARM instead of a 30-year fixed mortgage.

If you’re wondering how that shakes out in real dollars and cents, here’s what Redfin says. According to their research, the typical buyer could save about $150 per month by taking out an ARM instead of a 30-year fixed mortgage.

For some people, that’s enough to make a difference.

More Buyers Are Choosing Adjustable-Rate Mortgages Today

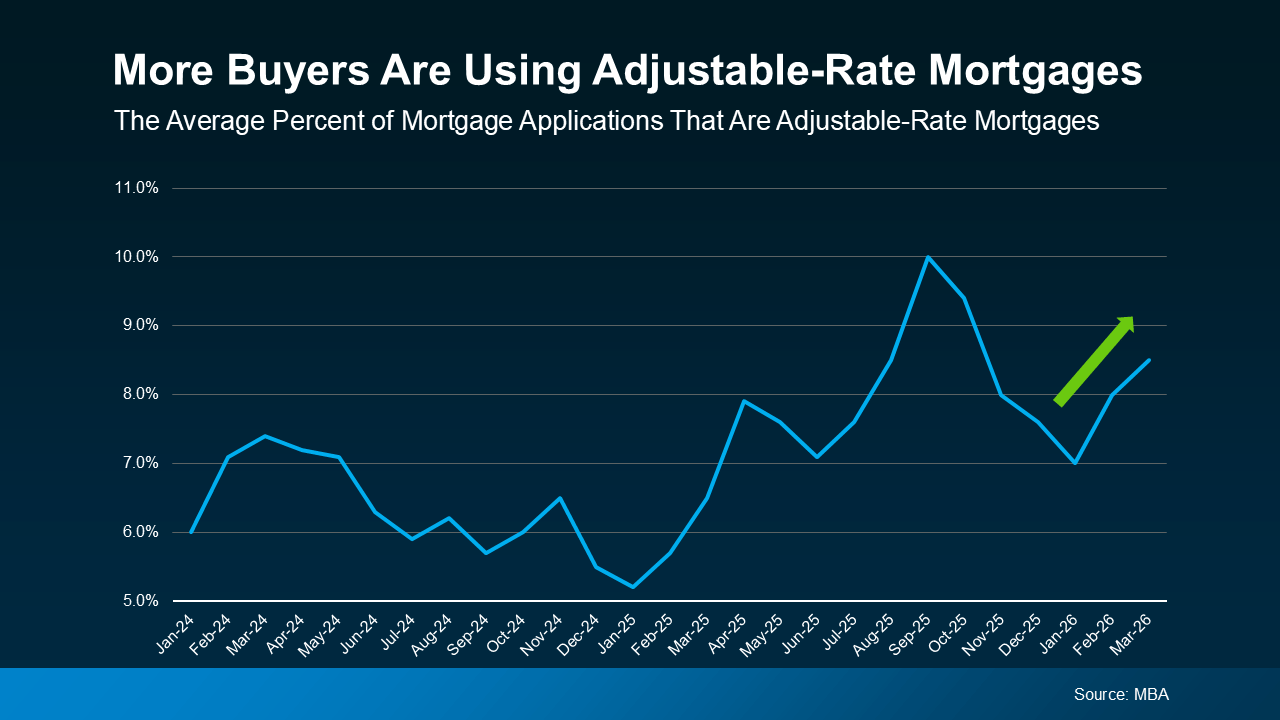

A growing number of buyers are willing to trade the uncertainty later for a lower payment now. Data from the Mortgage Bankers Association (MBA) shows the share of buyers choosing ARMs has increased, especially over the last few years (see graph below).

This doesn’t mean ARMs are becoming the go-to option for everyone. It only means some buyers are opting for this type of mortgage, so they can still buy today.

And if you remember the housing crash, seeing ARMs gain popularity again may raise concerns. But rest easy. Today’s ARMs aren’t the same.

And if you remember the housing crash, seeing ARMs gain popularity again may raise concerns. But rest easy. Today’s ARMs aren’t the same.

Back then, some buyers were given loans they couldn’t afford once rates adjusted.

Today, lending standards are stricter, and lenders evaluate whether borrowers could still handle the payment if rates rise. So, the return of ARMs doesn’t signal another widespread crash. It just reflects how some buyers are adapting to today’s affordability challenges.

The Trade-Off – What You Need To Consider

If you’re considering an adjustable-rate mortgage yourself, just remember it really all depends on your situation and your risk tolerance.

An ARM may make sense if you plan to move before your rate would adjust or if you expect you’ll make a higher income in the future. But there are trade-offs you need to think through.

For example, once the fixed period ends, your rate can adjust, and your payment could increase, potentially by a meaningful amount depending on where rates are at that time.

And keep in mind, there’s also no guarantee mortgage rates will come down in the future, which means refinancing later isn’t always an option. That’s why it’s important to think through your plan, understand your long-term earning potential, and work closely with a trusted lender before you choose an ARM.

Bottom Line

ARMs are getting more attention again because they can make buying a home more affordable in the short term. But they’re not right for everyone.

The key is understanding how they work, what the risks are, and whether they fit your plan. And that’s why you need to talk to a trusted lender and financial advisor before you make any decisions.

Mortgage rates have been volatile lately. And if you’re thinking about buying a home, that can make it harder to plan. But there are still things you can do to get the best rate possible in today’s market. It starts with having the right information.

So, what’s causing the bumps in rates? And what can you do about it? Let’s break it down.

Mortgage Rate Volatility Is Normal

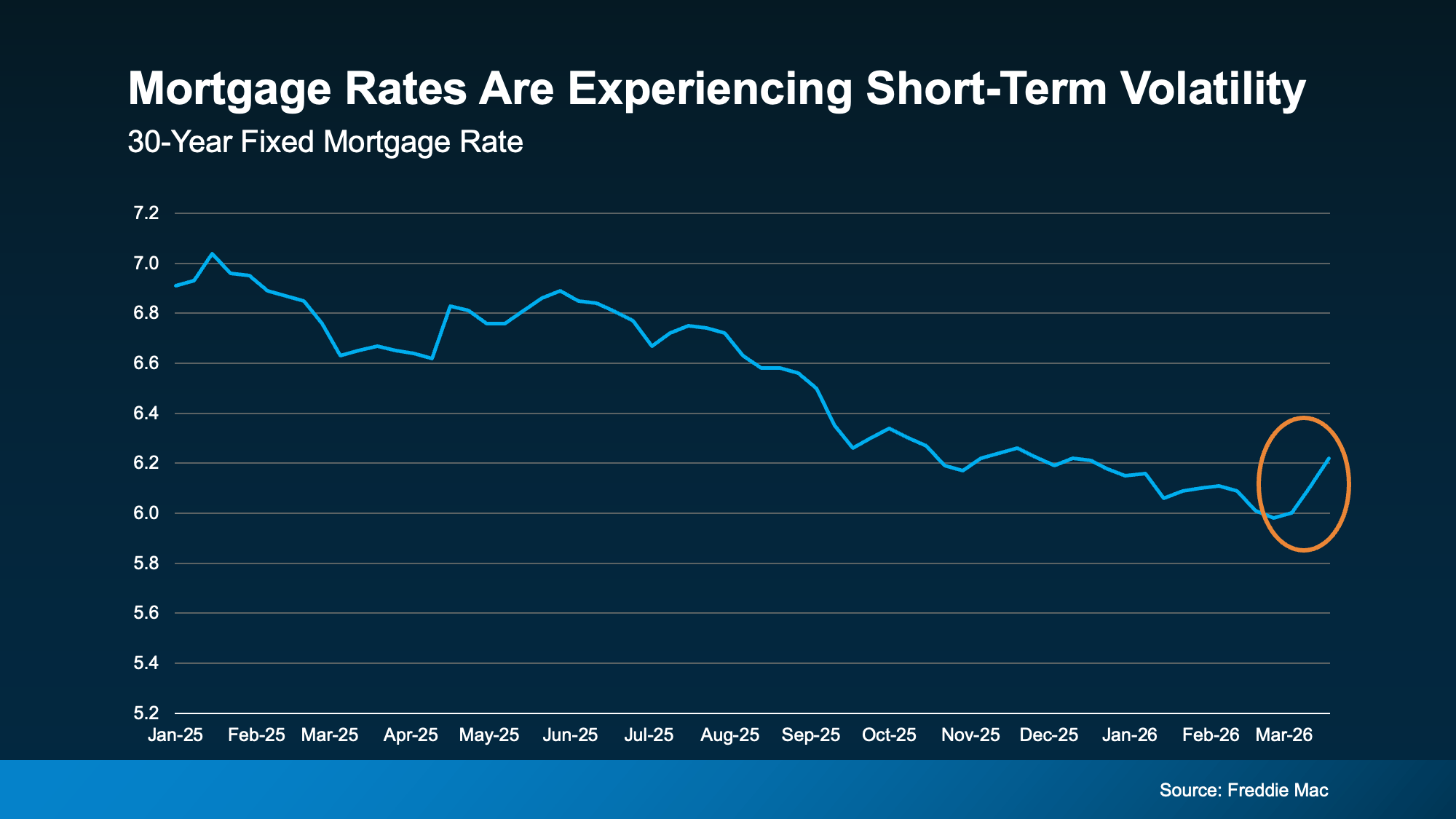

Data from Freddie Mac shows the recent volatility. After trending down for well over a year, there was a rise this month (see graph below):

While it’s easy to be distracted by the changes, here’s what you need to remember.

It’s normal for rates to bounce around a bit here and there. For example, if you look back at the graph, you’ll see that even within the past year there have been times like this when rates inched up. We’re in one of those moments right now and you need to be aware of that.

Especially when there’s economic uncertainty or big global events happening, volatility like this is expected. As Investopedia explains:

“Mortgage rates don’t move in isolation. When global events inject uncertainty into financial markets . . . that can ripple through to borrowing . . . mortgage costs can respond quickly to geopolitical developments. As long as uncertainty remains elevated, rate swings may continue.”

And that’s one of the reasons why trying to time the market isn’t a wise move.

You can’t control what happens with mortgage rates. But there are still things you can do to help you get the best rate possible in today’s market. And here’s where to focus your effort.

Your Credit Score

Your credit score plays a big role in the rate you qualify for. Even a small improvement can make a noticeable difference in your monthly payment. As Bankrate puts it:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

So, make sure you do what you can to keep your credit score up. If you’re not sure what your score is or how you can improve it, talk to a trusted loan officer.

Your Loan Type

There are also different types of home loans – and each one can have unique requirements, benefits, and rates for qualified buyers. The Consumer Financial Protection Bureau (CFPB) explains:

“There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans. Lenders decide which products to offer, and loan types have different eligibility requirements. Rates can be significantly different depending on what loan type you choose.”

That’s why it’s so important to explore your options with a lender. You may even want to talk to multiple lenders to see how the options vary.

Your Loan Term

The length of your loan matters too. Most lenders typically offer 15, 20, or 30-year loans. Freddie Mac offers this advice:

“When choosing the right home loan for you, it’s important to consider the loan term, which is the length of time it will take you to repay your loan before you fully own your home. Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

Again, to figure out what makes the most sense for your budget and long-term goals, have a lender walk you through all your options.

Bottom Line

Thinking about buying right now? The best advice is to accept that you can’t control where rates are going to go from here.

What you can do is work with a trusted lender and take steps that’ll help you get the best rate possible.

So, if you want to move today, talk to an agent and a lender to make it happen. You just need to control the controllables and focus where it counts.

The Secret To Selling Fast, No Matter the Market

4 Ways To Give Your Offer an Edge This Spring

Is Late May the Best Time To List Your House?

-

Affordability4 weeks ago

Affordability4 weeks agoWhen Buying a Home Feels Out of Reach, Some Families Do This Instead

-

Buying Tips4 weeks ago

Buying Tips4 weeks agoThinking About an Adjustable-Rate Mortgage? Here’s What You Need To Know.

-

Agent Value2 days ago

Agent Value2 days agoStay or Sell? How To Make the Right Call as You Age

-

For Buyers2 days ago

For Buyers2 days agoMore Options Are Popping Up This Spring

-

Affordability2 days ago

Affordability2 days agoThink You Have To Put 20% Down? Most First-Time Homebuyers Don’t.

-

Affordability2 days ago

Affordability2 days agoThe 10 Best Markets for First-Time Buyers This Spring

-

Equity2 days ago

Equity2 days agoRent or Buy? The Real Tradeoff Most People Don’t Talk About

-

Featured2 days ago

Featured2 days ago3 Things That Are Not Going To Happen in Today’s Housing Market

You must be logged in to post a comment Login