First-Time Buyers

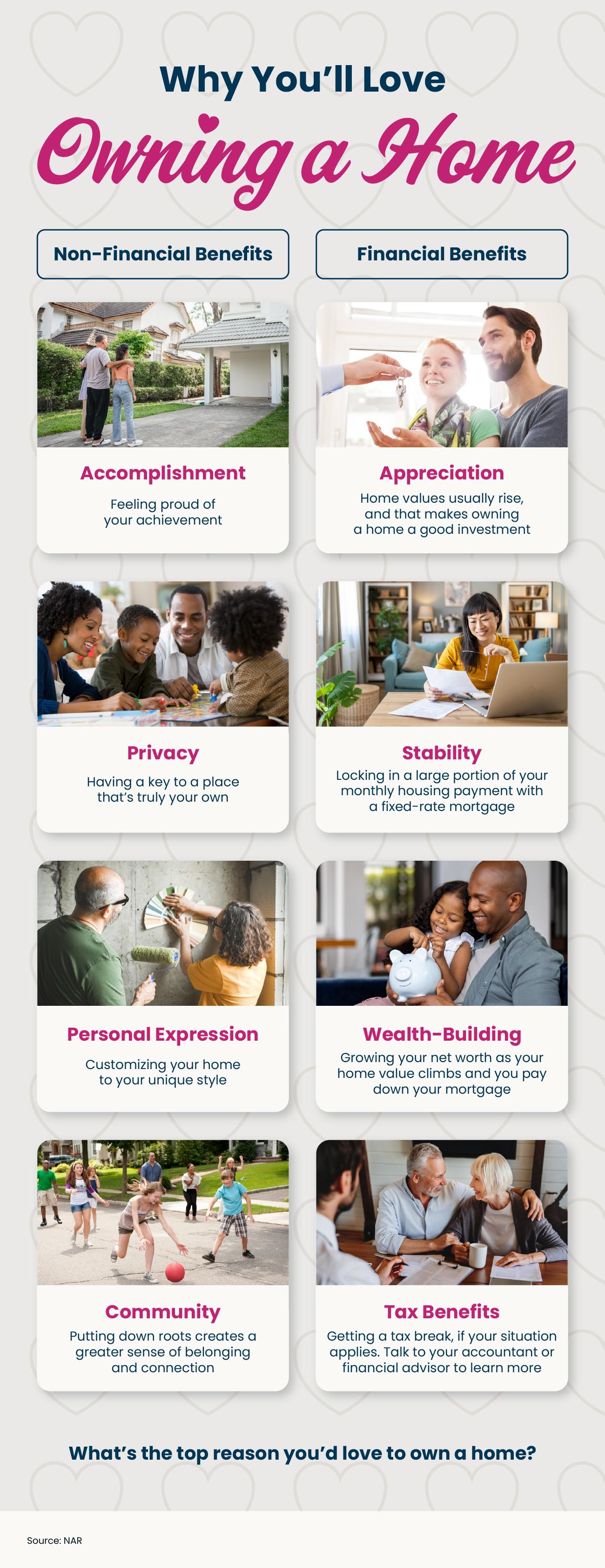

Why You’ll Love Owning a Home

Some Highlights

- Owning a home comes with many benefits, both non-financial and financial.

- From the sense of accomplishment and freedom of expression, to growing your net worth, it’s easy to fall in love with homeownership.

- What’s the top reason you’d love to own a home? Connect with an agent to come up with a plan that makes it possible.

For a lot of would-be first-time buyers, affordability is the thing that’s standing in the way. But some buyers are getting creative and finding a way to still make the numbers work – and that’s through co-buying.

The Dream Is Still Alive. The Math Just Isn’t Working for Everyone.

Young people haven’t given up on the dream of owning a home – not even close. According to FirstHome IQ, homeownership still ranks among the top life goals for the next generation.

The problem? 73% of Gen Z and millennial buyers cite affordability as the reason for not making homeownership a priority. And it shows. First-time buyers now make up just 21% of all home purchases, the lowest share since the National Association of Realtors (NAR) started tracking the data in 1981.

But still, some buyers are making it happen. And a portion of them are turning to co-buying to get their foot in the door.

So, What’s Co-Buying?

Co-buying means purchasing a home with someone else, like a friend, sibling, or unmarried partner. You combine incomes, split the down payment, and share monthly costs. For some people, it’s a creative way to turn “someday” into a concrete move-in date that’s just around the corner.

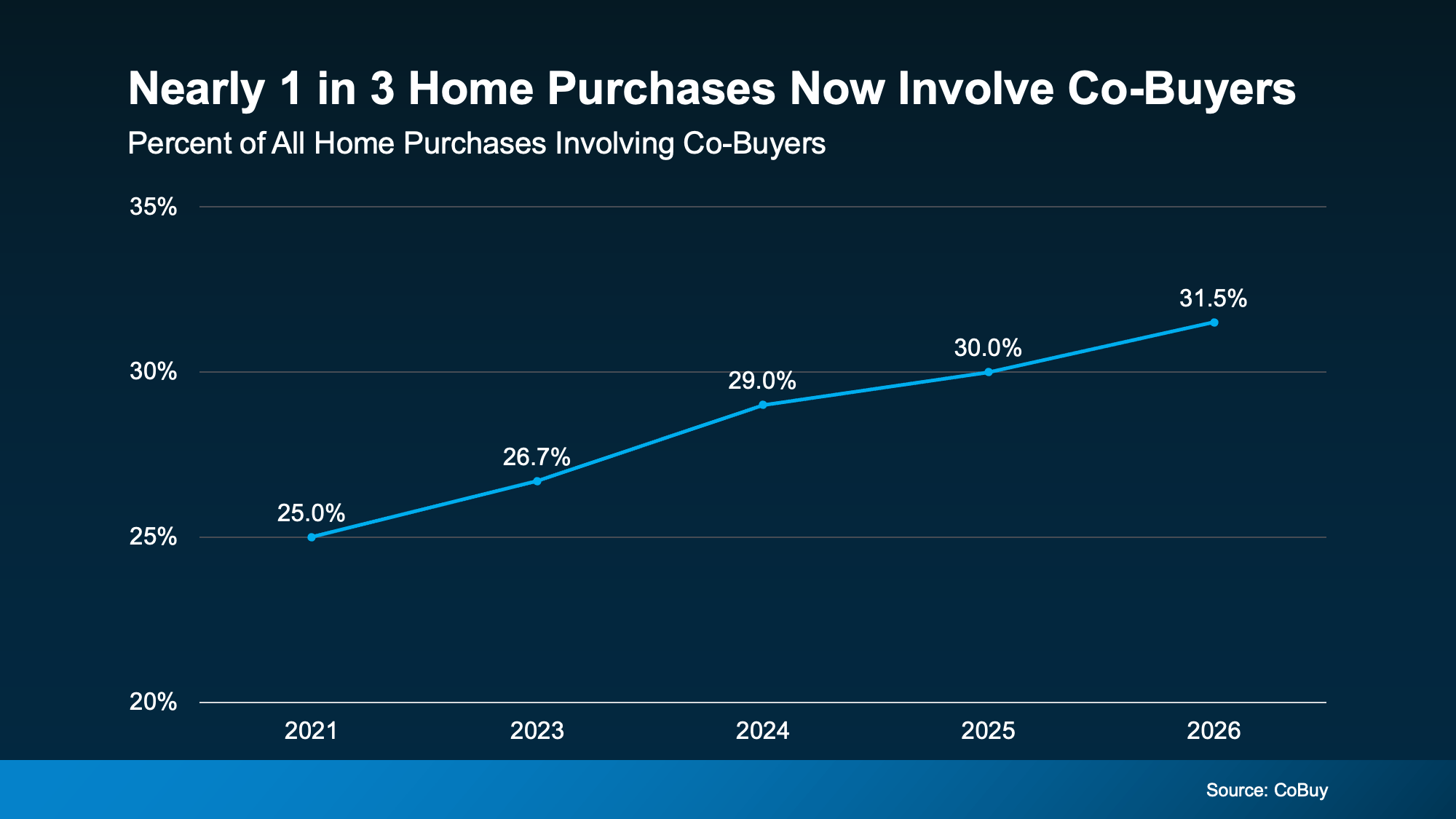

And it’s catching on fast, just look at where things stand today. According to CoBuy.io, 64 million Americans now co-own a home with someone they’re not married to. In fact, 31.5% of home purchases involve co-buyers (see graph below):

Why It Works

Why It Works

Here are just a few of the top reasons buyers are going this route, according to NerdWallet:

- Quicker path to homeownership: If owning a home is a serious goal for you, buying with someone else can help make that reality on a shorter timeline. Two or more people can save up a down payment a lot faster than one. That’s less time waiting and more time building equity in a place that’s yours.

- More purchasing power: With multiple incomes going toward the home purchase, you might be able to afford a nicer home or live in a more popular neighborhood. Sometimes teaming up means getting the home you actually want, not just the one you can barely afford on your own.

- Easier loan qualification: Added income from more than one buyer can also help with your debt-to-income (DTI) ratio, which the lender will calculate based on all the borrowers.

- Lower housing costs: Splitting up a mortgage payment multiple ways could maybe even make owning less expensive than renting. Plus, sharing costs can make repairs or renovations more manageable, too.

Things To Keep in Mind

If you’re considering going this route, there are some things you’ll want to think over. For starters, co-buying works best with people you trust and share financial goals with. So, before moving forward, make sure everyone agrees on how costs are split, who handles what, and what happens if one person wants to sell down the road.

That’s why a written co-ownership agreement can be a smart move. It keeps everyone on the same page and helps avoid headaches down the line. Think of it less like a legal formality and more like a game plan for your new investment.

Bottom Line

Affordability challenges are real, but they don’t have to mean waiting indefinitely. Co-buying is helping some first-time buyers stop waiting and start putting down roots.

If you’re curious whether it could work for your situation, talk with a local real estate agent. Reach out today and figure out your path to homeownership together.

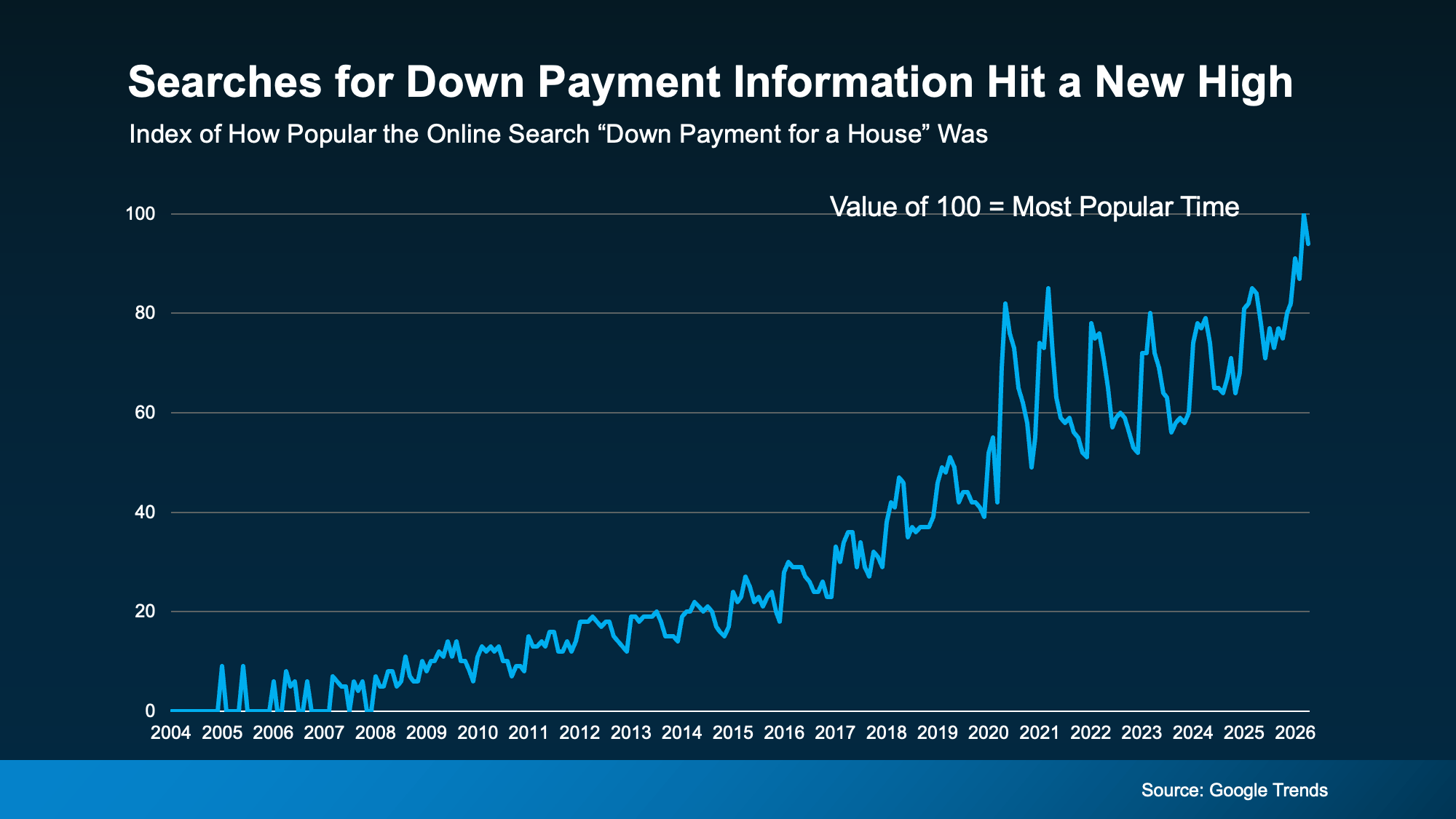

According to Google Trends, online searches for down payment information recently hit an all-time high. And that’s a clear sign more buyers are trying to figure out what they really need to save before making a move (see graph below):

If you’re wondering the same thing, you can always turn to the internet for answers. But a lot of the time, it’s better to ask a local expert. Because here’s what a pro would tell you.

If you’re wondering the same thing, you can always turn to the internet for answers. But a lot of the time, it’s better to ask a local expert. Because here’s what a pro would tell you.

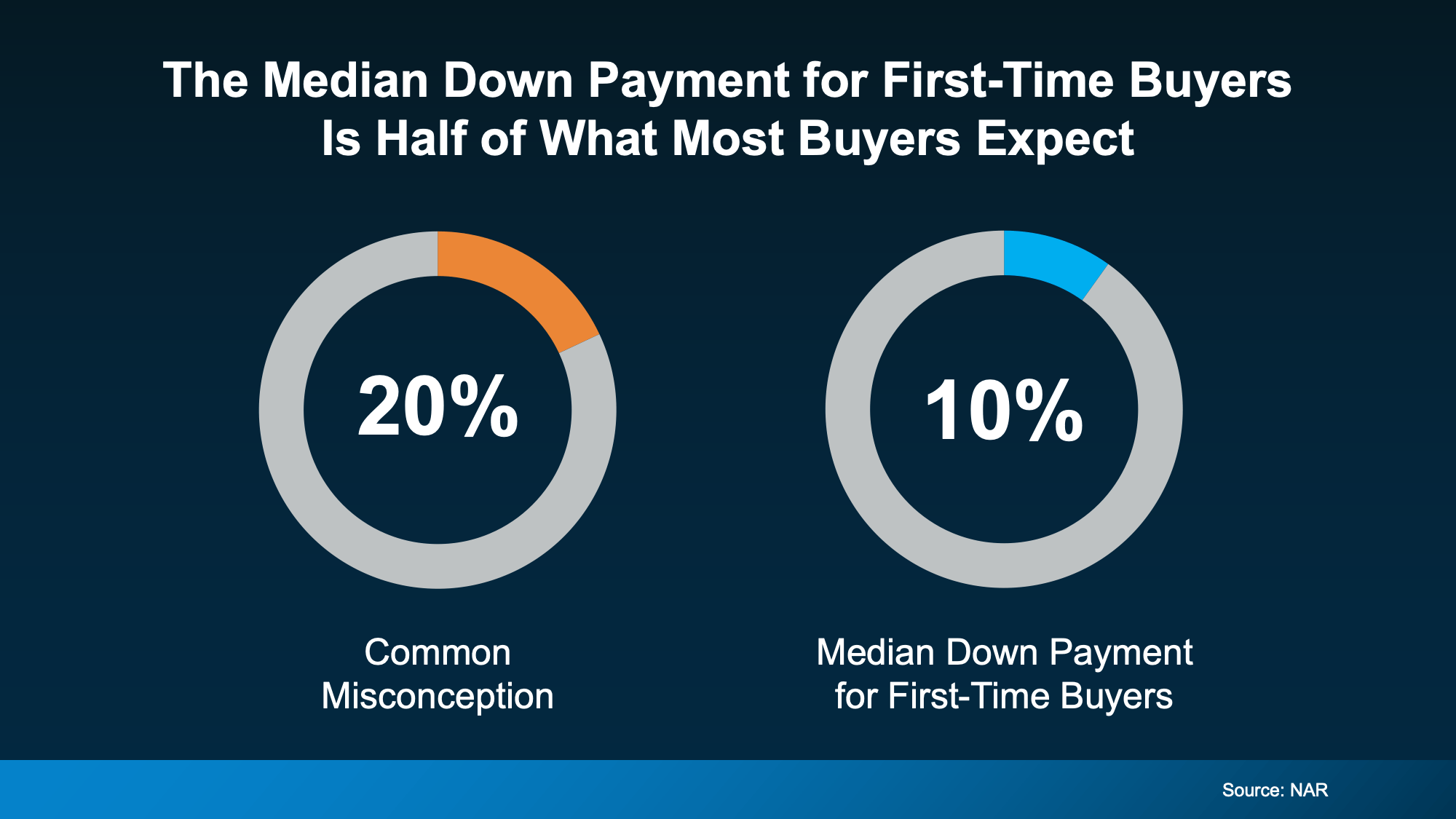

The 20% Down Payment Myth

The idea that you need 20% down to buy a home is one of the biggest misconceptions around the homebuying process. And the data debunks the myth.

While there are benefits to putting that much money down, most first-time buyers put down far less.

Here’s why. Unless it’s stated by your lender, you typically don’t have to have a 20% down payment. There are even some loan options designed to help you get into a home with a much smaller upfront cost. As the Mortgage Reports explains:

“The amount you need to put down will depend on a variety of factors, including the loan type and your financial goals. If you don’t have a large down payment saved up, don’t worry—there are plenty of options available, and you don’t need to put down the traditional 20% . . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . .”

For example, FHA loans allow down payments as low as 3.5%, while VA and USDA loans offer zero down payment options for qualified applicants, like Veterans.

And those options are just one reason so many first-time buyers are able to buy without a 20% down payment.

What Buyers Are Actually Putting Down

So, if buyers aren’t doing 20%, how much do they actually put down?

According to the National Association of Realtors (NAR), the median down payment for first-time homebuyers is only 10%. That’s half of what you probably expected.

That means if you’re aiming to save 20% because you think you have to, you may be setting a timeline that’s longer than necessary.

That means if you’re aiming to save 20% because you think you have to, you may be setting a timeline that’s longer than necessary.

And here’s some more good news. It’s not only that you may be able to buy with less money down than you thought, but there are also options to help you get to your down payment goal even faster.

Why You Should Look into Down Payment Assistance Programs

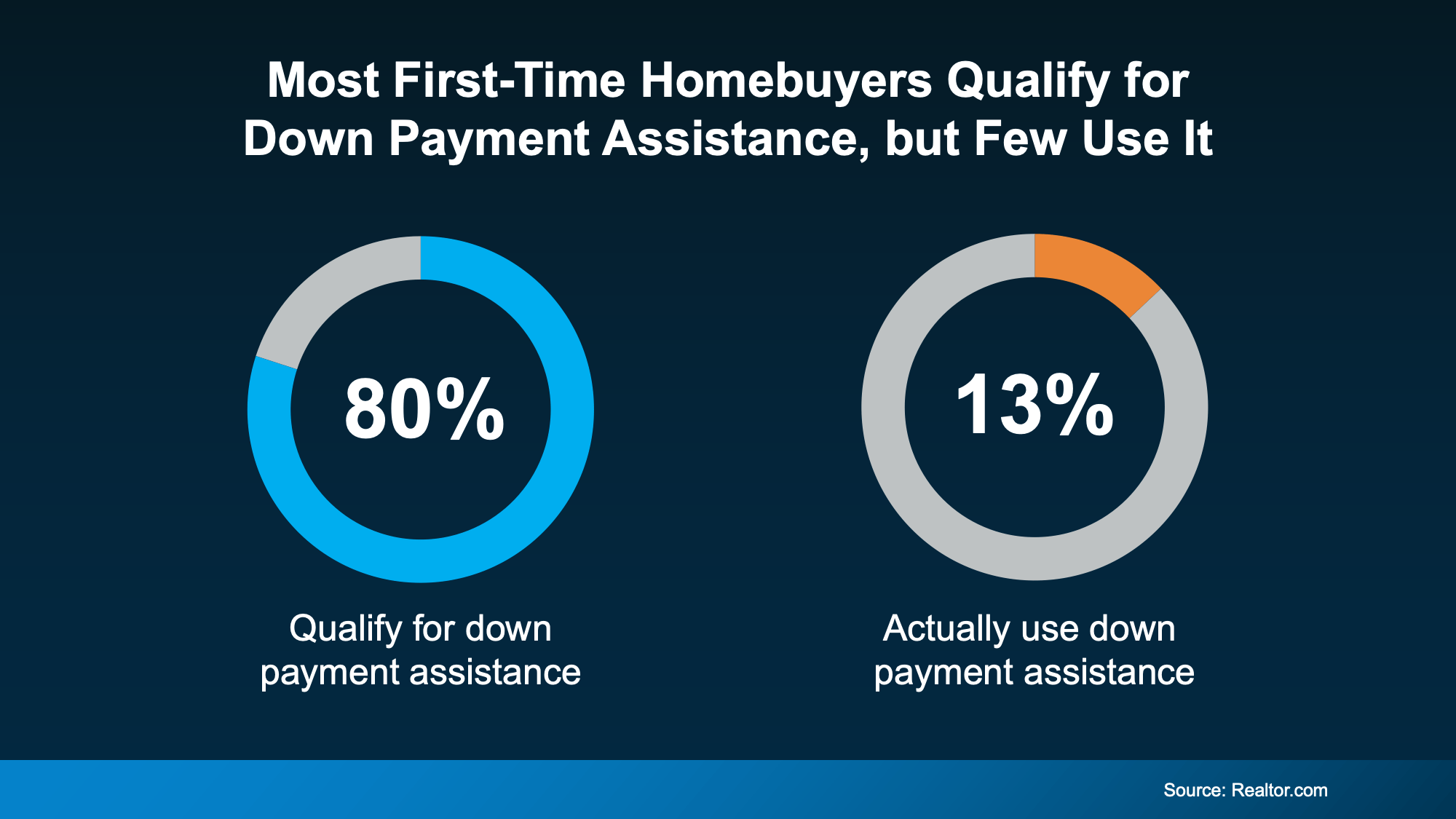

There are a lot of programs designed to help you save for a down payment – and they can make a big difference in how fast you hit your savings target. Unfortunately, buyers don’t realize how many there are, or that they may qualify for help.

Research from Realtor.com shows almost 80% of first-time homebuyers qualify for down payment assistance (DPA), but only 13% actually use it (see chart below):

And that’s another big miss holding would-be buyers like you back.

And that’s another big miss holding would-be buyers like you back.

In the U.S., there are over 2,600 homeownership programs available, many offering significant financial support. As Down Payment Resource shares:

“With an average benefit of $18,000, down payment assistance (DPA) remains one of the most essential tools for addressing the nation’s affordability challenges. Programs continue to expand in scope, serving a broader range of incomes, property types and borrower needs, including first-generation, military and repeat buyers.”

Imagine how much further your savings could go with an extra $18,000 you can use to buy. In some cases, you may even be able to stack multiple programs, giving what you’ve saved an even bigger boost.

Bottom Line

The simple truth is: most first-time buyers don’t put 20% down. And if you’ve been waiting to buy until you have that saved, you may be setting a timeline that’s longer than necessary.

To find out what you really need to save and if you qualify for any help, connect with a trusted lender who can walk you through your options. You may be able to buy sooner than you thought.

For a while, buying your first home hasn’t just felt hard. It may have felt out of reach.

Not because you weren’t ready.

Not because you weren’t trying.

But because every time you ran the numbers, they didn’t work.

That’s why so many first-time buyers stepped back.

But after years of sitting on the outside looking in, this Spring could give buyers like you an opening again – especially in some markets.

Metros Where Buyers May Have an Easier Time Breaking into the Market

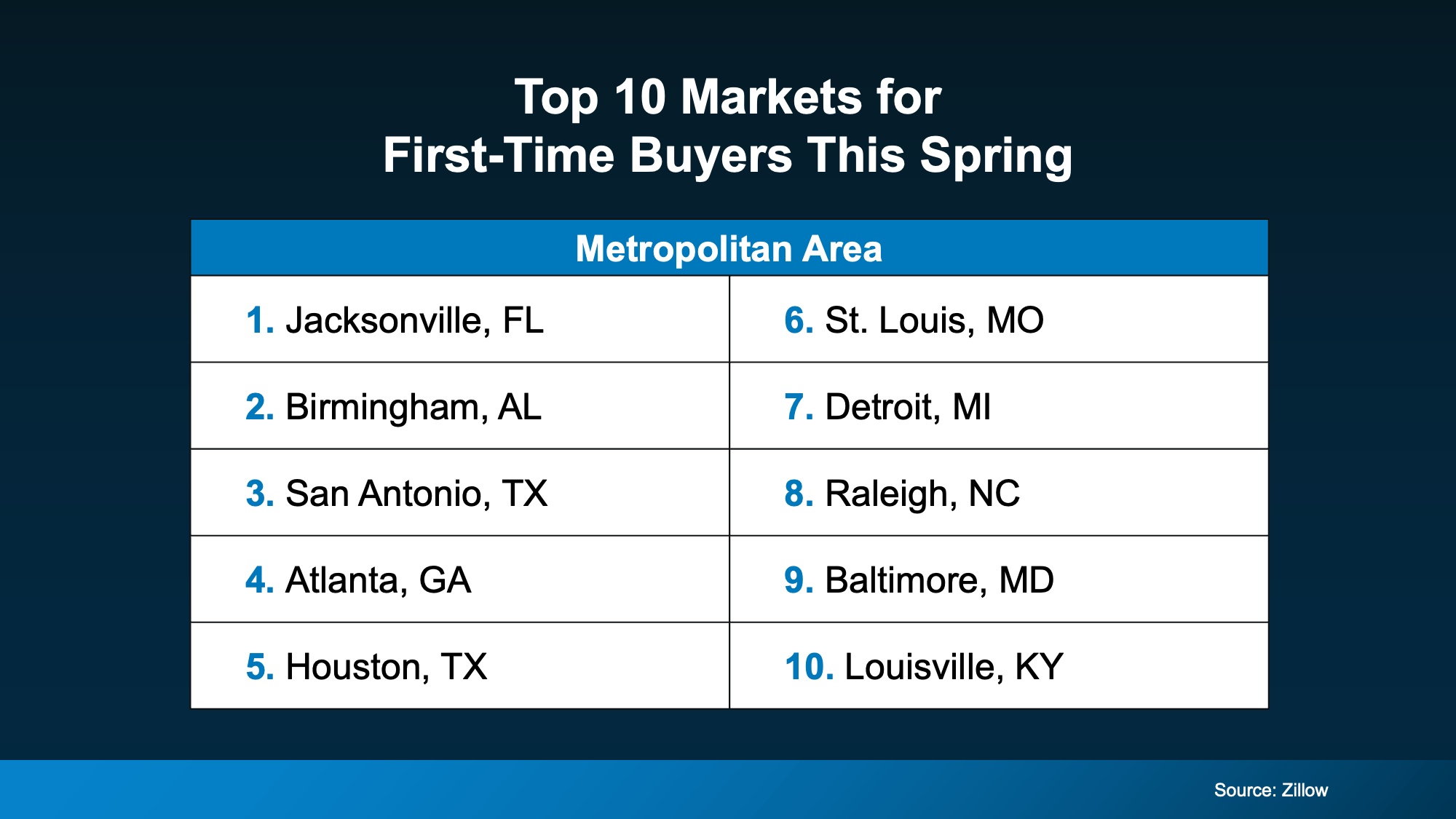

Zillow just released a list of the top 50 metros for first-time buyers this Spring. And here’s a quick snapshot of the top 10 (see chart below):

According to Zillow, in these top-ranked markets, median-income households can afford 68% of all homes for sale. Let that sink in.

Not long ago, it felt like you could barely afford anything.

Now, you may actually have some options again.

That doesn’t mean every home is suddenly going to fit your budget. But it does mean the door that felt closed for so many buyers is starting to crack back open. And in a number of cities, first-time buyers may finally be getting a shot at buying.

Why This Is Starting To Open Up

These cities are rising to the top not because of any one big change, but from a few smaller ones finally lining up. As Orphe Divounguy, Senior Economist at Zillow, explains:

“First-time buyers are finally seeing some light at the end of the tunnel. Affordability is still a challenge, but rising incomes, stabilizing prices and improving inventory are creating real opportunities in parts of the country. In the strongest markets for first-time buyers, they’ll find more choices, less competition and a clearer path to homeownership than they’ve had in years.”

Basically, three big things are working in your favor:

-

More homes are hitting the market. Realtor.com says inventory is up 8.1% compared to last year. That gives you more choices, less pressure, and more chances to find a place that fits your budget.

-

Price growth is moderating, so homes aren’t moving further out of reach as quickly. Some may even be falling back within your target price point.

-

Incomes are rising. If you make more money, that can offset some of the affordability challenges too.

And even though mortgage rates have been higher lately, that combination can still make a difference. As Mark Fleming, Chief Economist at First American, explains:

“Income growth has outpaced house price growth for 19 straight months, boosting house-buying power even as mortgage rates remain elevated.”

How To Find the Opportunities in Your Local Market

But what if your city didn’t make the top 10 list, or even the top 50 markets? Here’s what you really need to remember.

There’s going to be opportunities in every market, if you know where to look.

Even in the same city, two buyers can have completely different experiences. And a big part of that is who they choose as their partner. The right agent knows how to find pockets of opportunity in any market. That could mean:

-

A neighborhood where prices haven’t climbed as quickly

-

A part of town with more inventory, or

-

A new build community offering incentives so builders can sell their inventory

So, even if your city didn’t make the list, that’s okay. There’s still an opening for you, you just need your agent to help you find it.

Bottom Line

For a long time, first-time buyers have felt stuck, waiting for their turn to buy. But for some buyers, this Spring might be the first time in a while where things start to feel more within reach again.

Want to see which neighborhoods could give you the best shot at buying right now? Talk to a local agent.

The Pricing Mistake That Could Cost You Your Sale

What the Foreclosure Headlines Aren’t Telling You

Why Staging Your House Could Pay Off This Spring

-

Affordability1 week ago

Affordability1 week agoCould Co-Buying Be the Answer for Some First-Time Buyers?

-

Featured2 weeks ago

Featured2 weeks ago3 Things That Are Not Going To Happen in Today’s Housing Market

-

Equity2 weeks ago

Equity2 weeks agoRent or Buy? The Real Tradeoff Most People Don’t Talk About

-

For Buyers2 weeks ago

For Buyers2 weeks agoMore Options Are Popping Up This Spring

-

Agent Value2 weeks ago

Agent Value2 weeks agoStay or Sell? How To Make the Right Call as You Age

-

Affordability2 weeks ago

Affordability2 weeks agoThink You Have To Put 20% Down? Most First-Time Homebuyers Don’t.

-

For Sellers2 weeks ago

For Sellers2 weeks agoIs Late May the Best Time To List Your House?

-

Affordability2 weeks ago

Affordability2 weeks agoThe 10 Best Markets for First-Time Buyers This Spring

You must be logged in to post a comment Login