Buying Tips

Is an Accessory Dwelling Unit Right for You? Here’s What To Know

Are you having a hard time finding the right home in your budget? Or maybe you already own a home but could use some extra income or a designated space for aging loved ones. Either way, accessory dwelling units (ADUs) could be the smart solution you’ve been looking for in today’s market.

What Is an ADU?

According to Fannie Mae, an ADU is a small, separate living space that’s on the same lot as a single-family home. It must include its own areas for living, sleeping, cooking, and bathrooms independent of the main house. And they can take shape in a few different ways. Fannie Mae adds, an ADU can be:

- Within a main home, such as a basement apartment

- Attached to a main home, such as a living area over a garage

- Detached from the home entirely; it could even be a manufactured home

The Benefits of ADUs

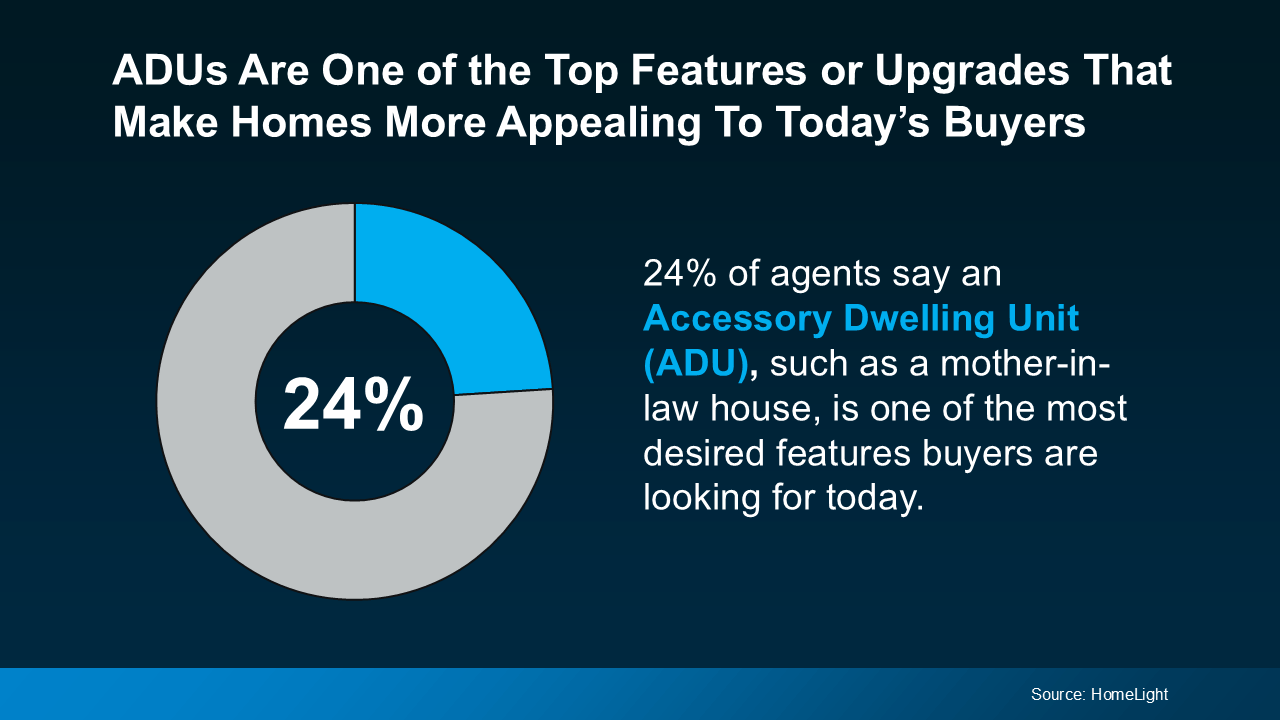

ADUs are growing in popularity as more people discover why they’re so practical. In fact, a recent survey shows that 24% of agents say an ADU, such as a mother-in-law house, is one of the most desired features buyers are looking for right now.

The growing appeal makes sense. With rising costs all around you, an ADU can help supplement your income and ease some of the strain on your wallet. Whether you buy a home that has one already or you add one on, it gives you the option to rent out that portion of your home to help pay your mortgage.

The growing appeal makes sense. With rising costs all around you, an ADU can help supplement your income and ease some of the strain on your wallet. Whether you buy a home that has one already or you add one on, it gives you the option to rent out that portion of your home to help pay your mortgage.

Here are some of the other top benefits of ADUs, according to Freddie Mac and the AARP:

- Living Close, But Still Separate: You get the best of both worlds — more quality time together, plus privacy when you want it. If that sounds like a win, it might be worth looking for a home with an ADU or adding one to your home.

- Aging in Place: Similarly, ADUs allow older people to be close to loved ones who can help them if they need it as they age. It’s a sweet spot that offers independence and support from loved ones. For example, if your parents are getting older and you want them nearby, this could be a great option for you.

- Built-In Childcare: If your family’s living in the ADU, you may be able to use them for childcare, which can also be a big cost savings. Plus, it gives your kids more time with their grandparents.

It’s worth noting that since an ADU exists on a single-family lot as a secondary dwelling, it typically can’t be sold separately from the primary residence. And while that’s changing in some states, regulations vary by location. So, connect with a local real estate expert for the most up-to-date guidance.

Bottom Line

In today’s market, buying a home with an ADU or adding one to your current house could be worth considering. Just be sure to talk with a real estate agent who can explain local codes and regulations for this type of housing and what’s available in your area.

What’s your motivation for exploring ADUs?

Mortgage rates have been volatile lately. And if you’re thinking about buying a home, that can make it harder to plan. But there are still things you can do to get the best rate possible in today’s market. It starts with having the right information.

So, what’s causing the bumps in rates? And what can you do about it? Let’s break it down.

Mortgage Rate Volatility Is Normal

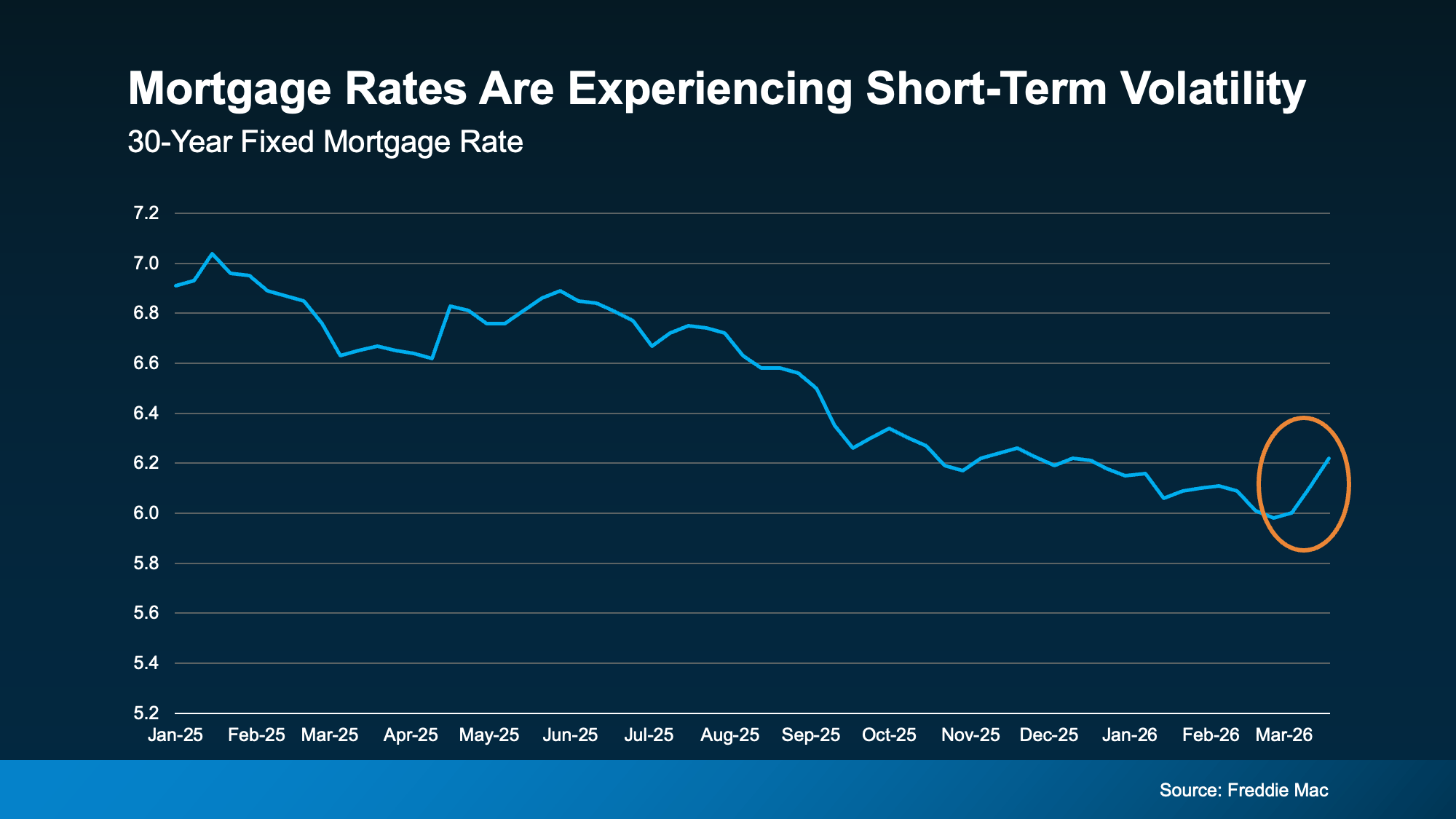

Data from Freddie Mac shows the recent volatility. After trending down for well over a year, there was a rise this month (see graph below):

While it’s easy to be distracted by the changes, here’s what you need to remember.

It’s normal for rates to bounce around a bit here and there. For example, if you look back at the graph, you’ll see that even within the past year there have been times like this when rates inched up. We’re in one of those moments right now and you need to be aware of that.

Especially when there’s economic uncertainty or big global events happening, volatility like this is expected. As Investopedia explains:

“Mortgage rates don’t move in isolation. When global events inject uncertainty into financial markets . . . that can ripple through to borrowing . . . mortgage costs can respond quickly to geopolitical developments. As long as uncertainty remains elevated, rate swings may continue.”

And that’s one of the reasons why trying to time the market isn’t a wise move.

You can’t control what happens with mortgage rates. But there are still things you can do to help you get the best rate possible in today’s market. And here’s where to focus your effort.

Your Credit Score

Your credit score plays a big role in the rate you qualify for. Even a small improvement can make a noticeable difference in your monthly payment. As Bankrate puts it:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

So, make sure you do what you can to keep your credit score up. If you’re not sure what your score is or how you can improve it, talk to a trusted loan officer.

Your Loan Type

There are also different types of home loans – and each one can have unique requirements, benefits, and rates for qualified buyers. The Consumer Financial Protection Bureau (CFPB) explains:

“There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans. Lenders decide which products to offer, and loan types have different eligibility requirements. Rates can be significantly different depending on what loan type you choose.”

That’s why it’s so important to explore your options with a lender. You may even want to talk to multiple lenders to see how the options vary.

Your Loan Term

The length of your loan matters too. Most lenders typically offer 15, 20, or 30-year loans. Freddie Mac offers this advice:

“When choosing the right home loan for you, it’s important to consider the loan term, which is the length of time it will take you to repay your loan before you fully own your home. Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

Again, to figure out what makes the most sense for your budget and long-term goals, have a lender walk you through all your options.

Bottom Line

Thinking about buying right now? The best advice is to accept that you can’t control where rates are going to go from here.

What you can do is work with a trusted lender and take steps that’ll help you get the best rate possible.

So, if you want to move today, talk to an agent and a lender to make it happen. You just need to control the controllables and focus where it counts.

Your House Hasn’t Sold Yet. Should You Rent It Out Instead?

Before You Fall in Love with a House, Do This First.

Don’t Let Home Prices Headlines Fool You

-

Agent Value4 weeks ago

Agent Value4 weeks agoIf Your House Isn’t Getting Offers, Read This.

-

Affordability4 weeks ago

Affordability4 weeks agoShould You Wait for Lower Rates?

-

Agent Value3 weeks ago

Agent Value3 weeks agoThe #1 Reason Buyers Walk Away (And How To Get Ahead of It)

-

For Buyers4 weeks ago

For Buyers4 weeks agoOne Key Sign We’re Not Headed for a Wave of Foreclosures

-

For Buyers7 days ago

For Buyers7 days agoDon’t Let Home Prices Headlines Fool You

-

Affordability3 weeks ago

Affordability3 weeks agoAffordability Has Improved in All 50 States

-

Agent Value3 weeks ago

Agent Value3 weeks ago3 Must-Do’s for First-Time Home Buyers

-

Equity2 weeks ago

Equity2 weeks agoThe Remodel You’ve Been Dreaming About May Be Closer Than You Think

You must be logged in to post a comment Login