Affordability

It’s Getting More Affordable To Buy a Home

There’s finally a little good news for anyone who’s been priced out or sitting on the sidelines.

Buying a home is getting more affordable.

Monthly payments have started to come down, and the squeeze buyers have been feeling for the past few years is slowly loosening. Now, that doesn’t mean everyone can suddenly afford a home, but with how tough the market’s been, the improvement we’re seeing matters.

Affordability Is Finally Moving in the Right Direction

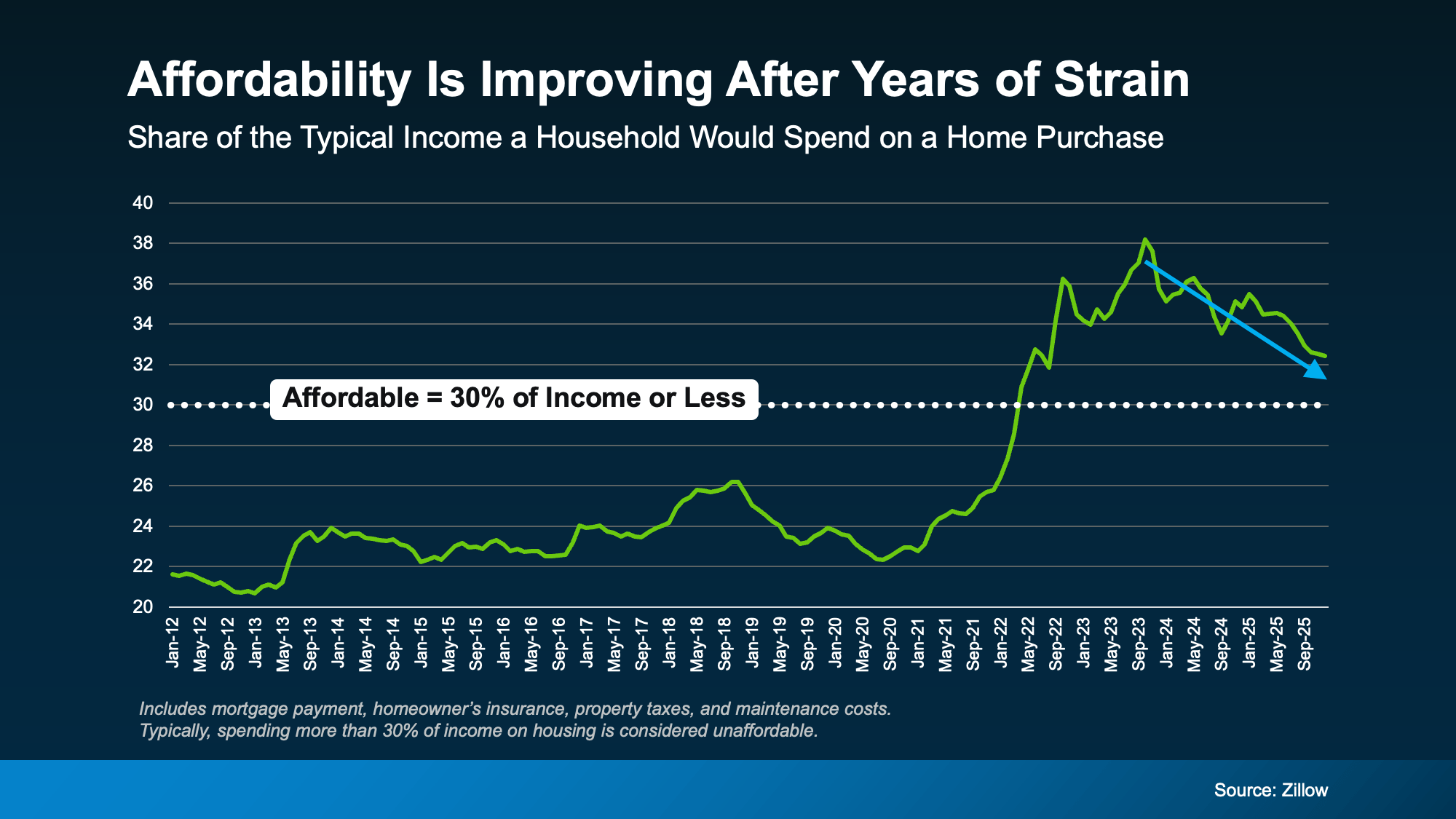

One of the best ways to see this shift is by looking at how much of a household’s income it takes to buy a home.

According to Zillow, housing is typically considered affordable when it takes 30% or less of your monthly income to cover your expenses. That includes your mortgage payment, taxes, insurance, and basic maintenance.

For the past few years, the math was well above that threshold, and it made buying a home unachievable for many. But now, we’re slowly moving back toward a balance. Zillow research shows it’s taking less of a typical household’s income to buy a home than it did just a few years ago (see graph below):

Now, we’re not all the way back to Zillow’s threshold of 30% of your income or less, so affordability is still tight. But things are trending in the right direction.

Now, we’re not all the way back to Zillow’s threshold of 30% of your income or less, so affordability is still tight. But things are trending in the right direction.

Why Affordability Is Improving

So, what’s driving the change? A lot of the focus lately has been on mortgage rates and how much they’ve come down over the course of the past year. But that’s not the only factor working in favor of buyers right now. Here are three trends benefiting buyers today:

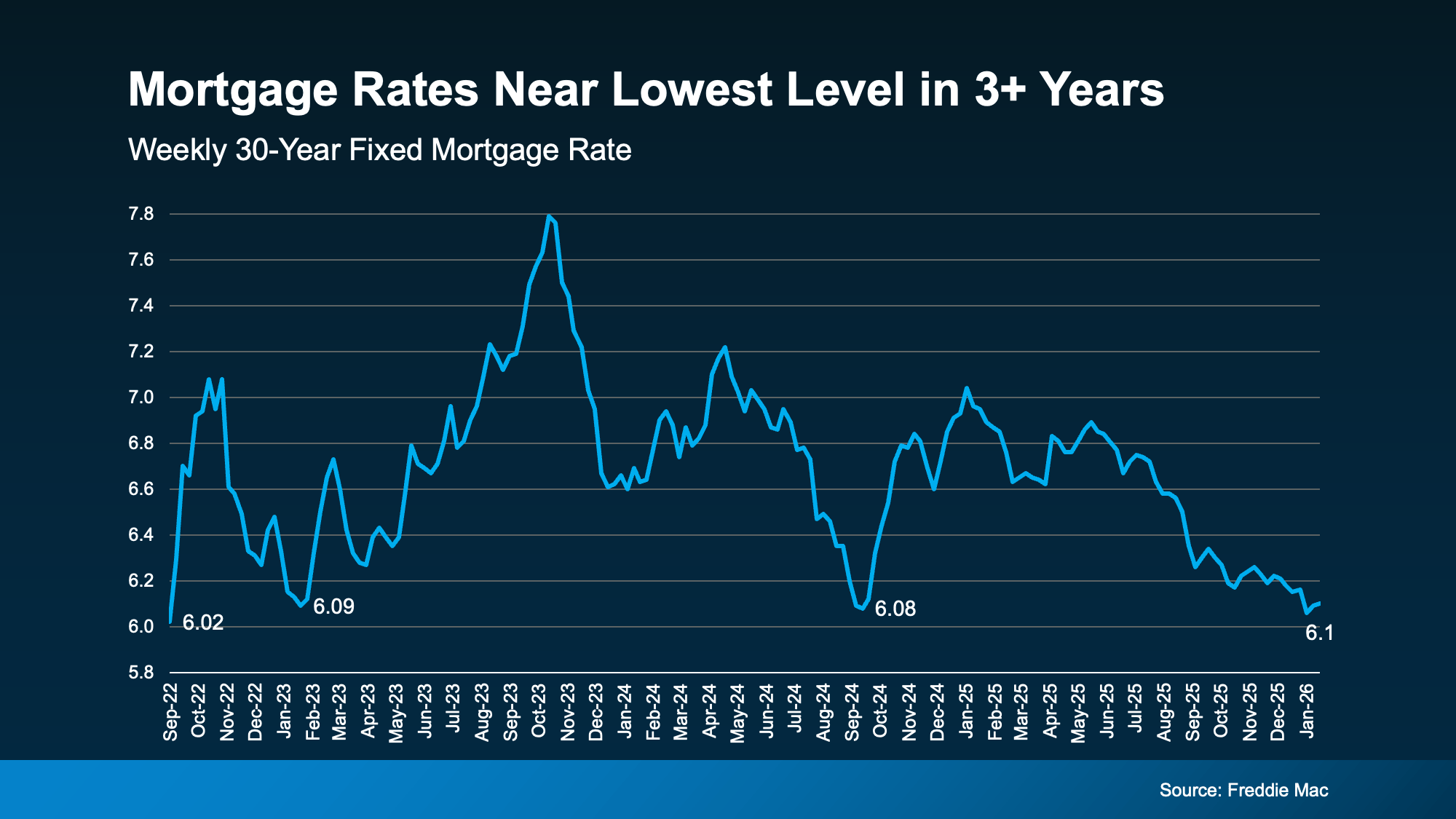

1. Mortgage rates have eased. Rates are near their lowest level in more than three years, which helps lower monthly payments (see graph below):

2. Home price growth has cooled. Prices aren’t falling nationally, but they’re growing much more slowly than they were a few years ago. That means buyers today aren’t facing the same sharp jumps in purchase prices, which helps keep monthly payments more manageable – and buying more predictable.

3. Wages are growing faster than home prices. This one matters a lot. As Mark Fleming, Chief Economist at First American, explains:

“When income growth exceeds house price growth, house-buying power improves—even if mortgage rates don’t decline meaningfully.”

None of this makes buying cheap, but it does explain why the math is starting to work a little better for buyers than it did even a just a year ago. Put simply, the forces that hurt affordability over the past few years are finally easing. Fleming again explains it well:

“Affordability remains challenging, but for the first time in several years, the underlying forces are finally aligned toward gradual improvement. Mortgage rates may drift down only slowly, but income growth exceeding house price appreciation will provide a boost to house-buying power — even in a higher-rate world. Affordability won’t snap back overnight, but like a ship finally catching a steady tailwind, it’s now sailing in the right direction.”

These three factors combined are why economists expect affordability to keep improving in 2026.

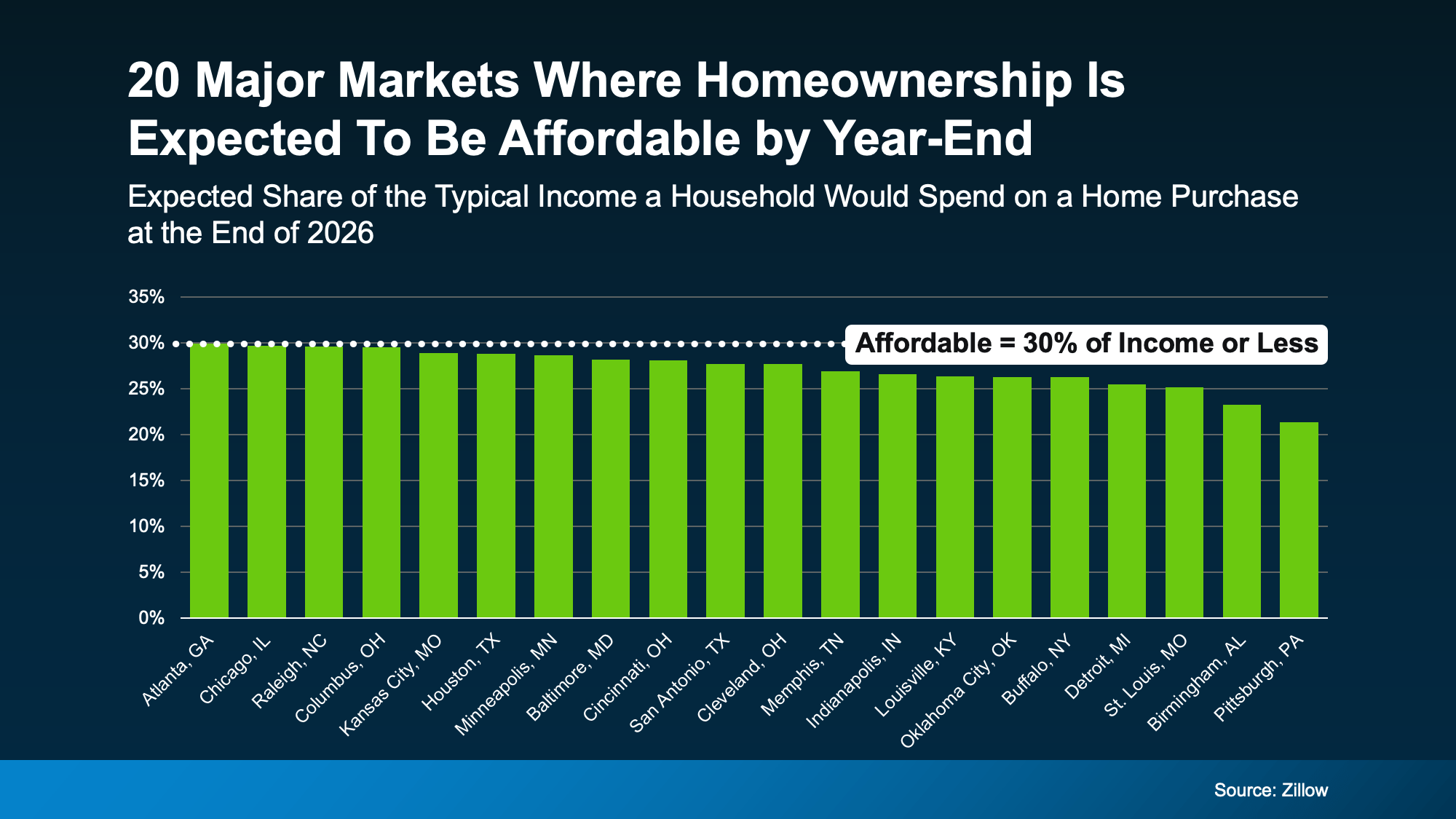

Where Homes Are Becoming Affordable First

But how much is affordability really going to improve? In some places, noticeably. Zillow says some markets are expected to fall back under their affordability threshold (30% of your income or less) by the end of the year:

But that doesn’t mean you have to be in one of these markets or wait until year-end to buy. Other places are already seeing big improvements in affordability. So, talk to a local agent about what’s happening in your market. You may find you’re able to buy after all.

Bottom Line

For the first time in quite a whole, affordability is easing. That’s a meaningful shift.

And because this improvement isn’t happening everywhere at the same speed, understanding what’s changing locally is what really makes a difference. If you want to see how these trends show up in your area, talk with a local real estate agent.

For a lot of people, the math on buying a home just doesn’t really work right now. Maybe that’s how it feels for you too. You look at the cost of buying. Then you look at the cost of childcare. And it starts to feel like you have to choose one or the other.

But some families are finding a way to make both work by doing something a little different: teaming up to purchase a multi-generational home.

One Reason This Is Becoming More Common

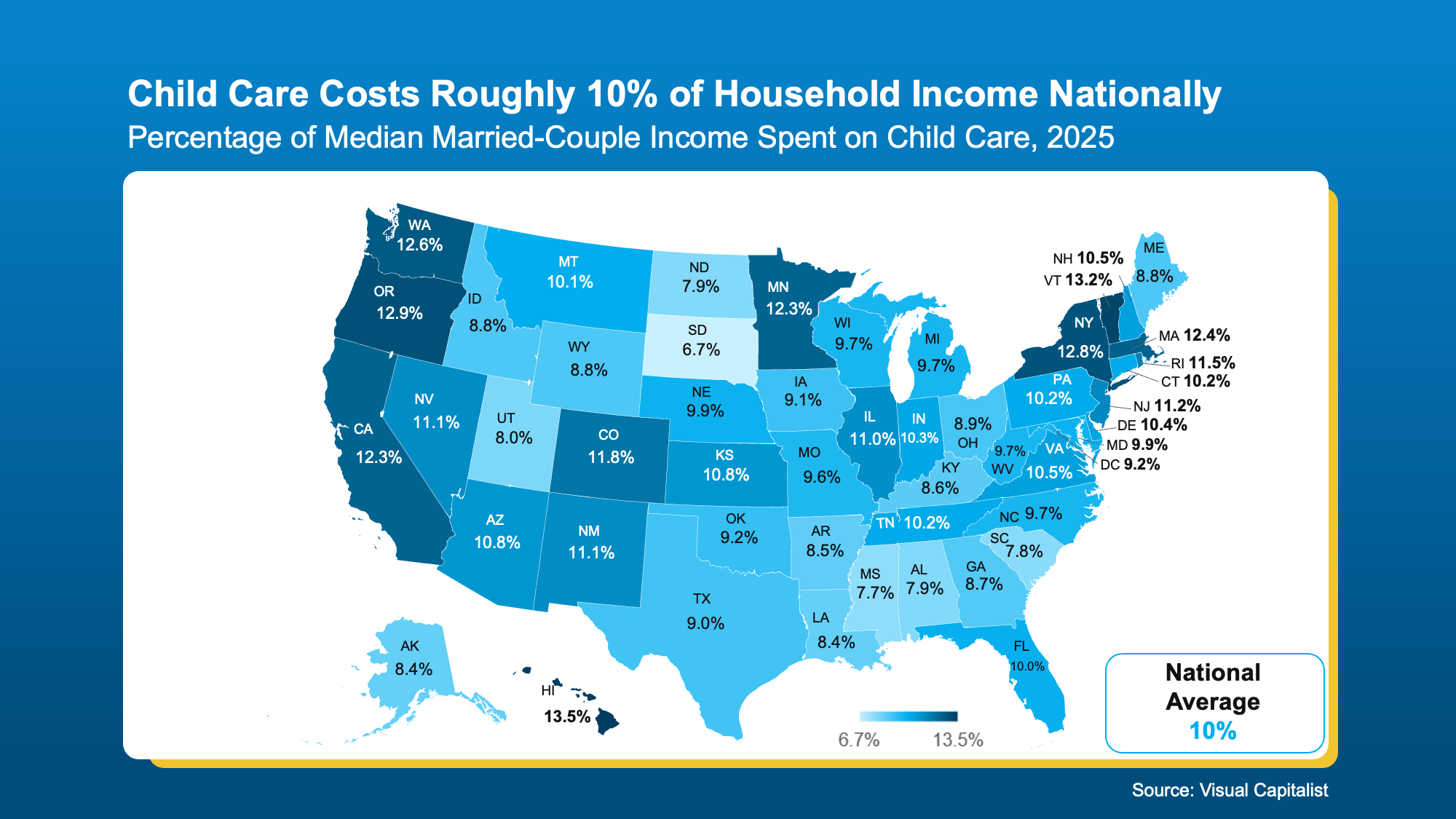

It’s no secret that affordability has been a challenge in recent years. But for families with young kids, there’s an added layer that can make it feel even harder: childcare.

According to the Department of Health and Human Services, childcare should take up no more than 7% of your monthly income. But in reality, the average married couple spends closer to 10% (see map below):

When you combine that with the cost of buying a home, it’s easy to see why things can feel stretched. That’s exactly why more families are starting to rethink how they approach both.

When you combine that with the cost of buying a home, it’s easy to see why things can feel stretched. That’s exactly why more families are starting to rethink how they approach both.

The Solution More People Are Turning To: Multi-Generational Living

One option gaining traction? Multi-generational living. That’s when parents, grandparents, or other relatives buy a house together and live under the same roof. And it’s not just about convenience anymore. It’s becoming a go-to strategy.

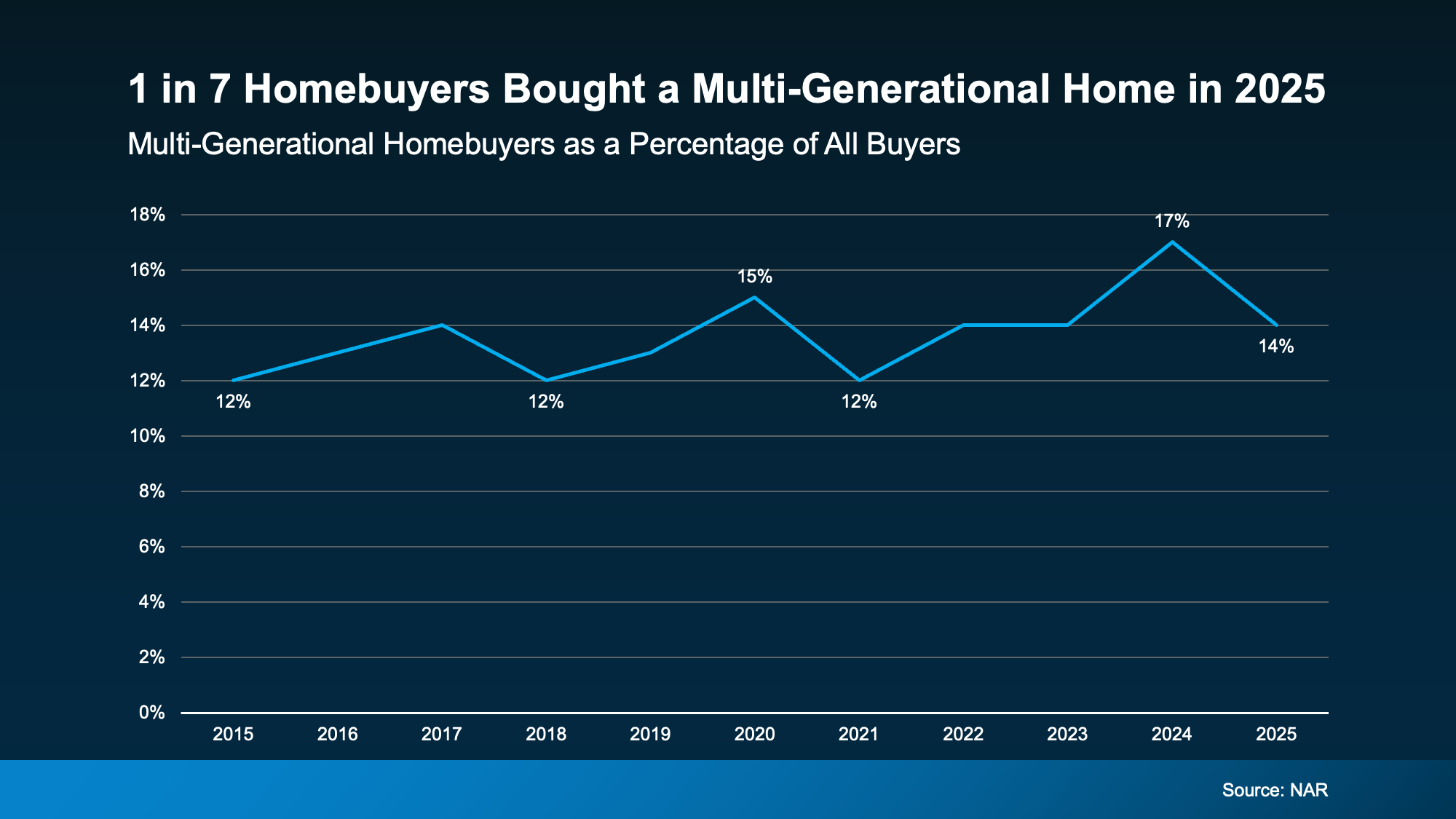

You can see it in the data. According to the National Association of Realtors (NAR), almost 1 in 7 homebuyers (14%) bought a multi-generational home in 2025 (see graph below):

And for the first time, childcare is showing up as a key reason why they chose this option. As NAR explains:

And for the first time, childcare is showing up as a key reason why they chose this option. As NAR explains:

“This year’s report features two new primary reasons for purchasing a multi-generational home: grandchildren living in the home (12%) and to help reduce the cost of childcare (6%).”

Why It Works

Buying a multi-generational home solves two big challenges at the same time.

- First, it shares the financial responsibility. If you pool multiple incomes together, you may be able to afford a home you couldn’t have on your own.

- Second, it can also solve the childcare puzzle. When grandparents or other relatives live in the home, they may be able to help with daily care – which can significantly reduce or even eliminate daycare costs.

And for many people, that combination is what finally makes their move possible.

If the costs of childcare and housing together have made buying feel out of reach right now, it may be worth exploring creative options like buying a home with your loved ones.

Bottom Line

If you want more information on multi-generational homes, talk to a local agent about what’s available in your area.

Sometimes the path to homeownership isn’t doing it alone. It’s doing it together.

For the past few years, affordability has been what’s stopped a lot of buyers in their tracks. Maybe it stopped you, too.

At some point you probably did the math, looked at the monthly payment, and decided to pause your search and wait for things to get better. But here’s something you may have missed while you’ve been sitting on the sidelines.

Over the last year, housing affordability has improved in all 50 states. Yes, you read that right. It’s gotten better in every single state.

That’s based on new research coming out of First American. And while housing is still fairly expensive compared to historical standards, the pressure buyers felt over the last few years is finally starting to ease.

Some Areas Are Seeing Bigger Improvements

The first thing you need to know is that this isn’t just happening in one region or in a small handful of cities. The trend is happening almost everywhere.

Sure, individual states, cities, and even neighborhoods are going to vary – sometimes by a lot. But overall, more buyers are able to buy again. And in 48 of the top 50 metros, affordability has improved over the past year.

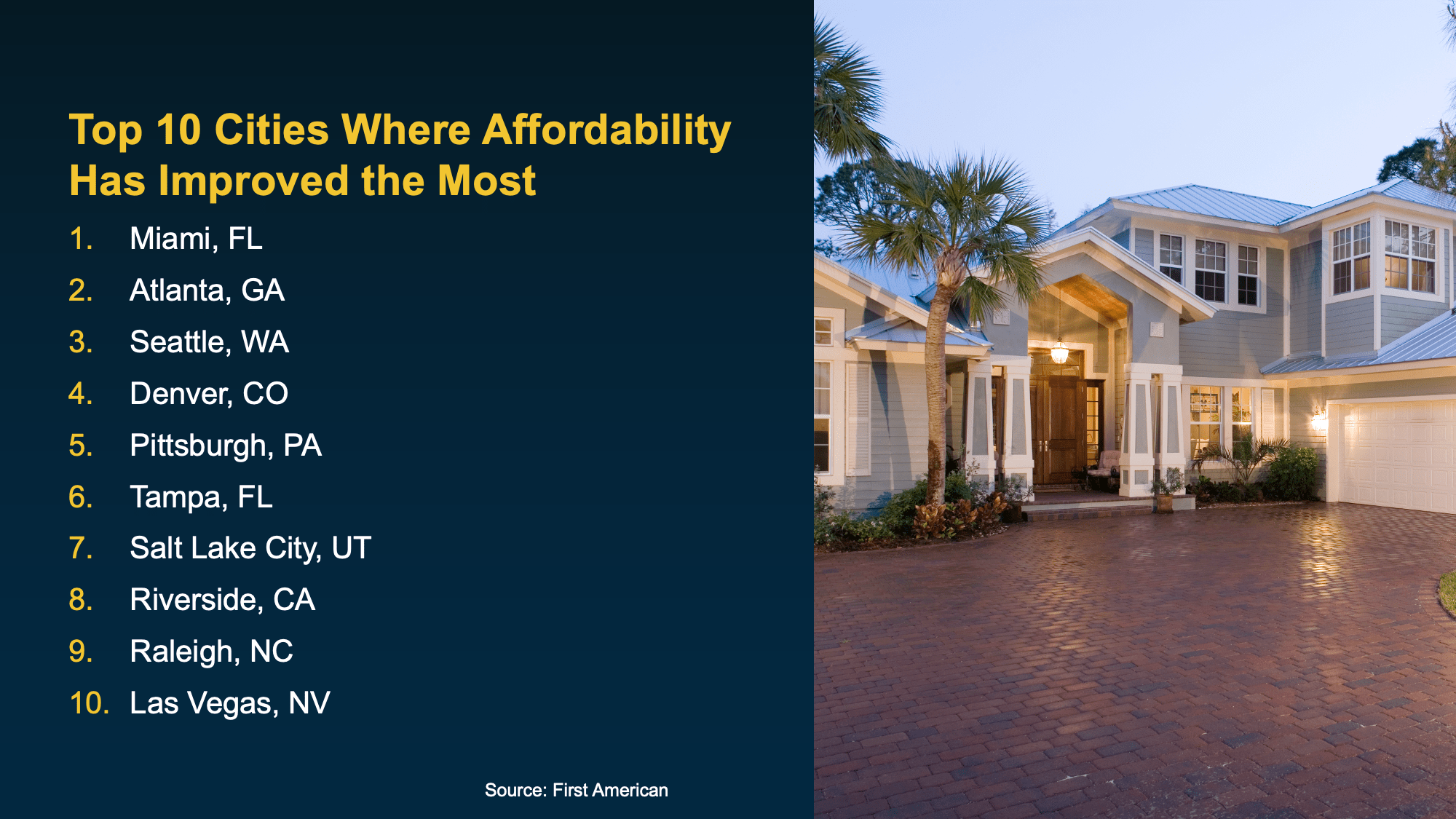

That same research breaks down which cities are seeing the biggest gains:

Just in case you’re wondering: why these areas? It’s simple. In many cases, it comes down to the number of homes for sale.

Just in case you’re wondering: why these areas? It’s simple. In many cases, it comes down to the number of homes for sale.

When buyers have more choices, it creates a healthier balance in the market and that can help bring affordability back within reach. With homes up for grabs, it opens the door a bit wider for buyers to negotiate with sellers for credits, price cuts, and more. And it gives you more chances to find a house that works for your needs and budget.

It may make more of a difference than you think.

None of this means affordability challenges have completely disappeared. Buying a home is still a big financial decision. But the trend is moving in a direction many buyers have been waiting for.

As Chen Zhao, Head of Economic Research at Redfin, puts it:

“The housing affordability crisis is showing signs of easing . . . opening the door for more Americans to make the jump to homeownership.”

Bottom Line

If you were holding off on buying, this could be exactly the signal you’ve been waiting so long for. To find out how much affordability’s improved in your area, connect with a local real estate agent.

Mortgage rates have already dropped into the upper 5s twice this year. But after just a few days, they ticked back up into the low 6% range. If you saw that and thought, “Great. I missed it,” you’re not the only one.

A lot of buyers are treating the 5s like some kind of magic number. As if moving from 6.1% to 5.99% suddenly changes everything. And from a mindset perspective, it does feel different.

But here’s the part most people don’t actually run the math on.

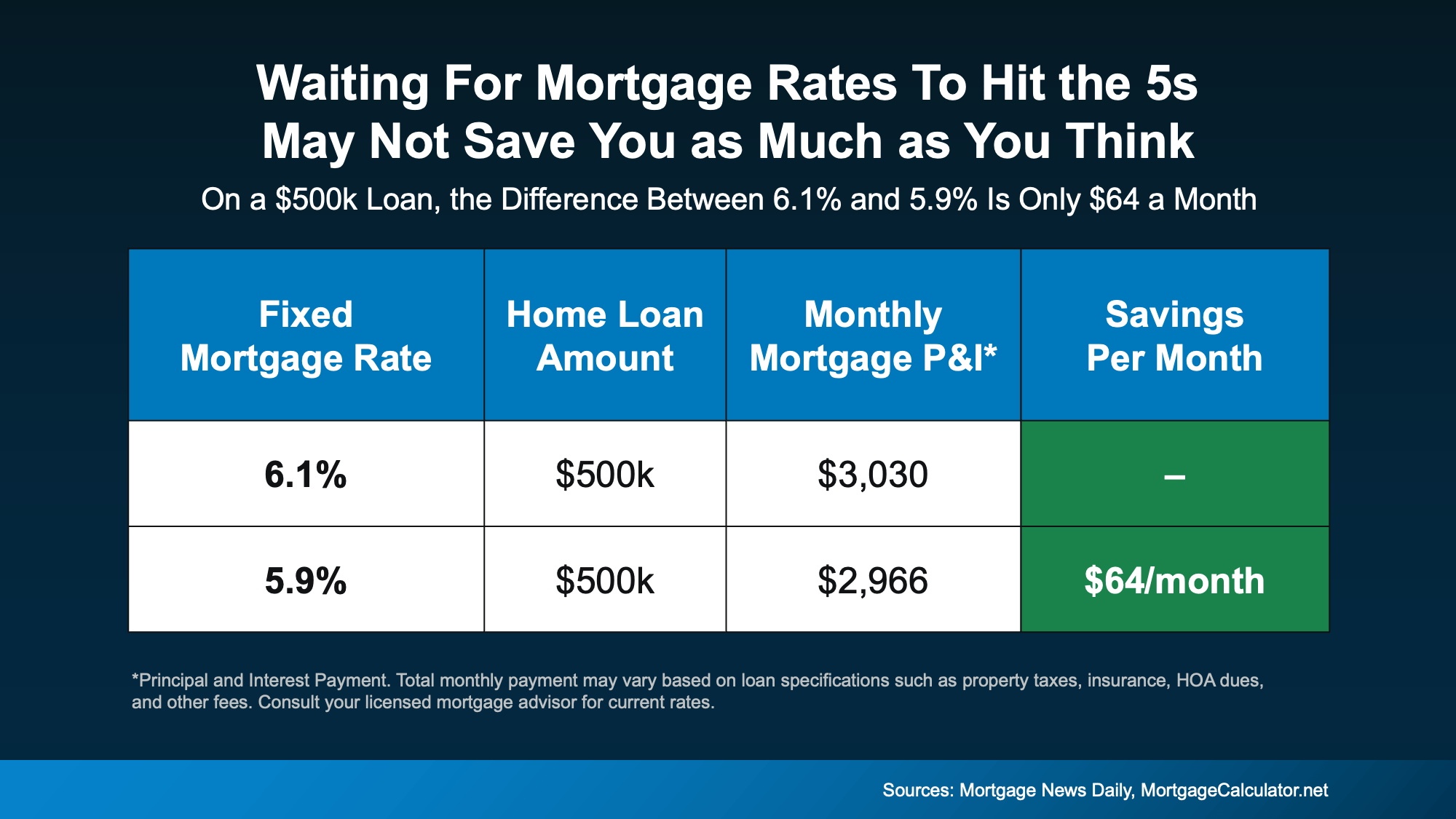

The Payment Difference Isn’t What You Think

Let’s say you’re looking at a $500,000 home loan. At 6.1%, generally speaking, your principal and interest payment is roughly $3,030 per month. At 5.9%, it’s about $2,966 per month.

That’s a difference of only $64 a month.

Not $300.

Not $500.

Sixty dollars.

Let that sink in for just a moment.

Yes, over time that $64 a month can add up. But it’s far from the dramatic swing many buyers imagine when they say they’re “waiting for the 5s.”

Yes, over time that $64 a month can add up. But it’s far from the dramatic swing many buyers imagine when they say they’re “waiting for the 5s.”

The psychological impact of seeing a 5 in front of your rate can feel big. The financial impact? It might be something you don’t even notice when it’s all said and done.

Experts Aren’t Predicting a Big Drop

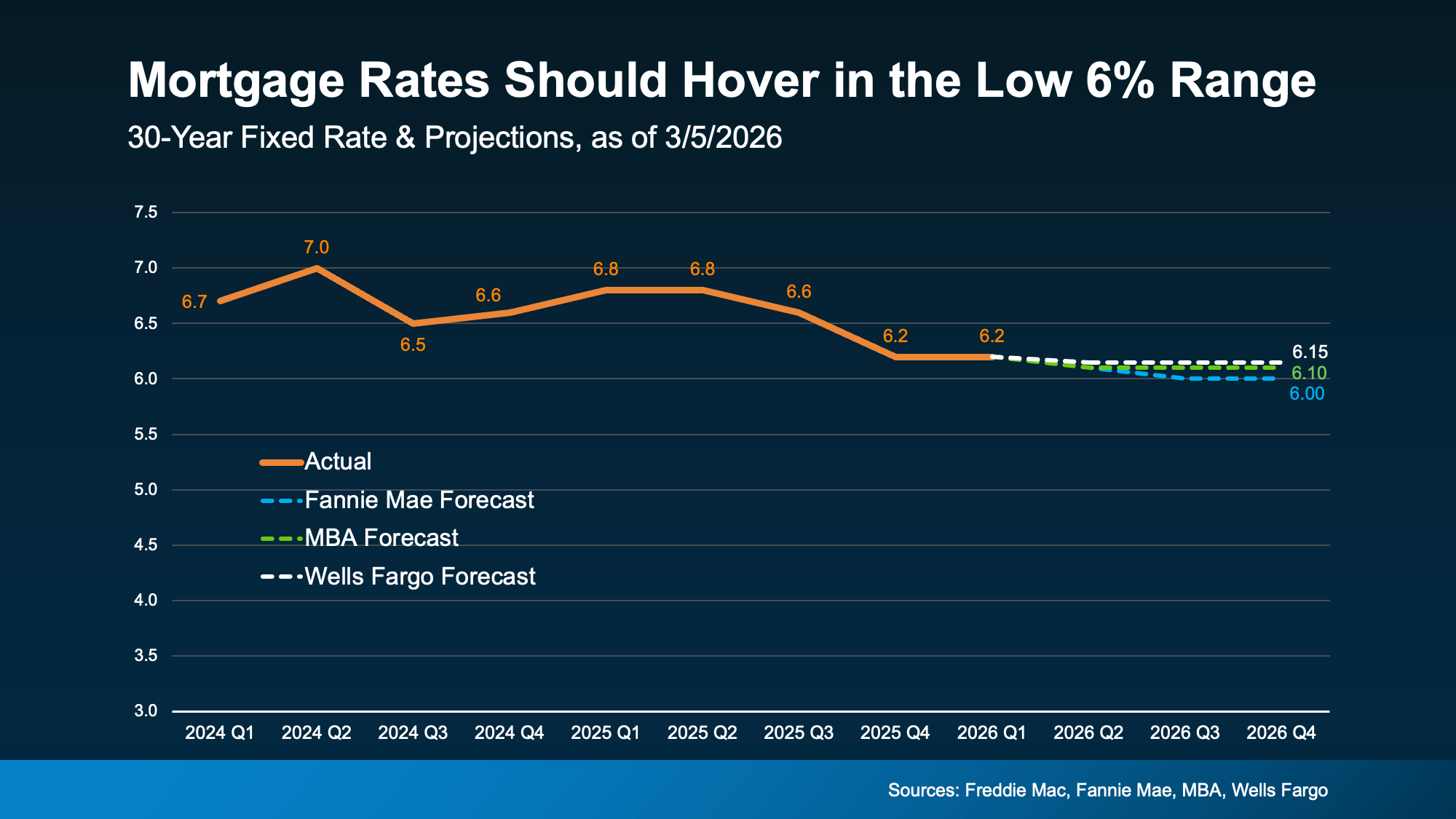

Another important piece to think about: most housing economists aren’t forecasting a long-term return to 5% territory anytime soon.

While rates will move up and down, likely hitting the high 5s here and there, the broader expectation is for mortgage rates to hover in the low 6% range this year, not stay in the 5’s or decline much more.

While it certainly could happen, the reality is, waiting for a deep drop may not deliver the payoff you’re hoping for, if you’re holding out

While it certainly could happen, the reality is, waiting for a deep drop may not deliver the payoff you’re hoping for, if you’re holding out

The Bigger Question to Ask

Instead of asking, “Did I miss the 5s?” A better question is: “Does today’s payment work for me?”

If the monthly payment fits comfortably in your budget, and you’ve found a home that meets your needs, the difference between 6.1% and 5.9% likely isn’t the deciding factor. It might be one of them, but it shouldn’t be everything.

And remember, mortgage rates aren’t permanent. If they drop meaningfully later, refinancing is always an option. But you can’t refinance a home you didn’t buy.

Waiting Might Feel Safe, But It Isn’t Always Strategic

It’s natural to want the best possible rate. Everyone does. But sometimes buyers overestimate how much a rate in the high 5s will change things in today’s market.

Don’t miss the fact that rates have already come down. A year ago, they were in the 7s. Now? They’re hovering in the low 6s. And for a lot of people, that percentage point difference that’s already here is the real game changer.

If you paused your plans when rates were higher, now may be the right time to re-run your numbers. Not because rates are “perfect.” But because the monthly payment math might work better than you think, even with rates in the low 6s.

Before assuming you’ve missed your moment, take another look at the numbers.

You may find it never disappeared.

Bottom Line

If you’ve been sitting on the sidelines waiting for that magic five number for rates, that strategy may not pay off as much as you’d expect.

Connect with an agent or lender so you can double check the math at your price point. You may realize payments are already within your range.

When Buying a Home Feels Out of Reach, Some Families Do This Instead

Thinking About an Adjustable-Rate Mortgage? Here’s What You Need To Know.

Your House Hasn’t Sold Yet. Should You Rent It Out Instead?

-

Agent Value4 weeks ago

Agent Value4 weeks agoIf Your House Isn’t Getting Offers, Read This.

-

For Buyers1 week ago

For Buyers1 week agoDon’t Let Home Prices Headlines Fool You

-

For Buyers4 weeks ago

For Buyers4 weeks agoOne Key Sign We’re Not Headed for a Wave of Foreclosures

-

Agent Value4 weeks ago

Agent Value4 weeks agoThe #1 Reason Buyers Walk Away (And How To Get Ahead of It)

-

Affordability3 weeks ago

Affordability3 weeks agoAffordability Has Improved in All 50 States

-

Agent Value3 weeks ago

Agent Value3 weeks ago3 Must-Do’s for First-Time Home Buyers

-

Buying Tips2 weeks ago

Buying Tips2 weeks agoYou Can’t Control What’s Happening with Mortgage Rates. But You Can Control This.

-

Equity3 weeks ago

Equity3 weeks agoThe Remodel You’ve Been Dreaming About May Be Closer Than You Think

You must be logged in to post a comment Login