Economy

History Shows the Housing Market Always Recovers

Now that the market is slowing down, homeowners who haven’t sold at the price they were hoping for are increasingly pulling their homes off the market. According to the latest data from Realtor.com, the number of homeowners taking their homes off the market is up 38% since the start of this year and 48% since the same time last June. For every 100 new listings in June, about 21 homes were taken off the market.

And if you’ve made that same choice, you’re probably frustrated things didn’t go the way you wanted. It’s hard when you feel like the market isn’t working with you. But while slowdowns can be painful in the moment, history tells us they don’t last forever.

History Repeats Itself: Proof from the Past

This isn’t the first time the housing market has experienced a slowdown. Here are some other notable times when home sales dropped significantly:

- 1980s: When mortgage rates climbed past 18%, buyers stopped cold. Sales crawled for years. But as soon as rates came down, sales surged back, and the market found its footing again.

- 2008: The Great Financial Crisis was one of the toughest housing downturns in history. Sales and prices both dropped hard. Still, sales rebounded once the economy recovered.

- 2020: During COVID, sales disappeared overnight, and many people had to put their plans on hold. Yet the recovery was faster than anyone expected, with a surge of buyers re-entering the market as soon as restrictions eased.

The lesson is clear: no matter the cause, the market always rebounds.

Today’s Situation: Where We Stand Now

Over the past few years, home sales have been sluggish. And one big reason why is affordability. Mortgage rates rose at a record-breaking pace in 2022, and home prices were climbing at the same time. That combination put buying out of reach for many people. And when demand slows, home sales do too.

The Outlook: Why Things Will Improve

But here’s the encouraging part. Forecasts show sales are expected to pick up again moving into 2026.

Last year, just about 4 million homes sold (shown in gray in the graph below). And this year is looking very similar (shown in blue). But the average of the latest forecasts from Fannie Mae, the Mortgage Bankers Association (MBA), and the National Association of Realtors (NAR) show the experts believe there will be around 4.6 million home sales in 2026 (shown in green).

And a big reason behind that projection is the expectation that mortgage rates will come down a bit, making it easier for more buyers to jump back in.

That means what’s happening now is part of a cycle we’ve seen before. Every slowdown in the past has eventually given way to more activity, and this one will too.

That means what’s happening now is part of a cycle we’ve seen before. Every slowdown in the past has eventually given way to more activity, and this one will too.

Just like the 1980s, 2008, and 2020, today’s dip in home sales is temporary.

What That Means for You

If you’ve paused your moving plans, you did what you thought was right. Your frustration is valid. But it’s also important to remember the bigger picture. Housing slowdowns don’t last forever.

That’s where your local real estate agent comes in. Their job is to keep a close eye on the market for you. When the first signs of a rebound appear, they’ll help you spot the shift early so you can relist with confidence.

Bottom Line

If today’s housing market feels stuck, remember it’s never stayed down for good. Slowdowns end, activity returns, and people get moving again. So, connect with a local real estate agent, because when the next wave of buyers shows up, you won’t want to miss it.

As activity picks up again, will you be ready to put your house back on the market, or do you need to move sooner?

Homebuyers are watching the economy closely, and for good reason. Buying a home is one of the biggest purchases most people ever make. And some recession talk in the media has made a lot of would-be buyers second guess their plans.

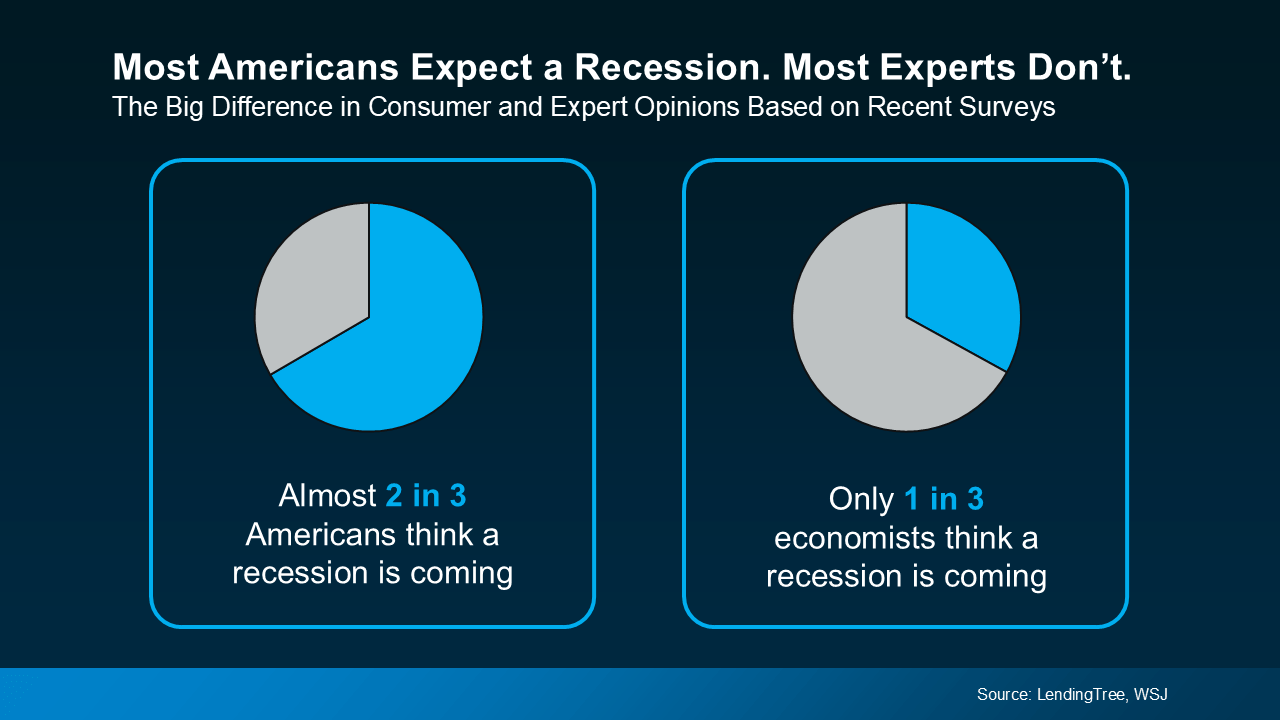

In the latest LendingTree survey, almost 2 in 3 Americans said they think a recession is coming. And 74% of respondents say that’s having an impact on their financial decisions.

But here’s the good news: the experts aren’t nearly as concerned.

Most Americans Expect a Recession, But Most Experts Don’t

According to an October report from the Wall Street Journal (WSJ), only 1 in 3 experts surveyed say we may be headed for a recession sometime in the next 12 months (see graph below):

If the expert economists aren’t super worried, should you be? We’re not in a recession right now. And there’s no guarantee we’re heading into one.

If the expert economists aren’t super worried, should you be? We’re not in a recession right now. And there’s no guarantee we’re heading into one.

What we do have is uncertainty – and the best way to handle that is by leaning on facts, not fear. You can do that by making sure you have the information you need to make an informed decision.

Tips for Buying a Home During Periods of Economic Uncertainty

Here’s the best advice anyone can give right now. While it’s important to keep an eye on what’s happening in the economy, that shouldn’t necessarily overshadow your real-life needs. Economic shifts come and go, but the reasons people buy homes rarely change. Danielle Hale, Chief Economist at Realtor.com, explains:

“Well-prepared buyers who have been waiting on the sidelines are likely motivated by personal and lifestyle needs like growing families, new jobs, or retirement. And these considerations can outweigh short-term economic uncertainties . . . ”

Timing your move around real life (not the news cycle) is what matters most.

But here’s the key. If you’re going to buy a home right now, job stability really matters. You need to feel confident in your income and know you can comfortably manage your mortgage payments, even if your situation or the economy shift.

If your job is secure and you’ve built a cushion of savings, experts say you don’t necessarily need to delay. Just keep these tips from the economists at Redfin in mind:

- Set a budget and stick to it: Don’t overextend. Make sure your payments are affordable and your savings can cover any surprises. This includes factoring in costs likely to rise, like home insurance and taxes.

- Negotiate: There are more homes for sale right now, and other buyers may pull back because of their own fears. That gives you more negotiating power when working with sellers. Use it to get the best deal possible.

- Be strategic about payments and mortgage rates: Talk to lenders about what payment you can afford and the rate you can qualify for today, as well as your options if rates go down later on.

- Consider selling before you buy: If you already own a home, selling first can reduce the financial pressure and help solidify your budget for your next home.

But nothing replaces the value of having a trusted team around you, especially right now. As Bankrate says:

“Buying a home during a recession can sometimes be a good idea – but only for people who are lucky enough to remain financially stable . . . Be sure to enlist the help of an experienced local real estate agent. Not only do agents know their markets well, they will also work to get you the best deal in any given situation, including a recession.”

Bottom Line

Most Americans think a recession is coming. But most experts don’t.

So, you don’t necessarily have to put your moving plans on hold. If your finances are solid, your job is stable, and you have a real need to move, you can still make this happen. You just need the right team of pros by your side.

What’s holding you back from making your next move? Connect with a local agent and lender to talk it over.

There’s been a lot of talk lately about how a government shutdown impacts the housing market. You might be wondering: Is it causing everything to grind to a halt?

The short answer? No.

The housing market doesn’t stop. It keeps moving. Homes are still being bought and sold, contracts are still being signed, and closings are still happening. The difference is that a few parts of the process may slow down a little, but overall, the market continues to function.

Here’s What Typically Happens

Whenever the government shuts down, some federal agencies temporarily close or scale back their operations. That can cause a few hiccups in real estate, especially when it comes to processing certain types of government loans and insurance requirements:

- “Applicants for FHA, VA, or USDA loans—which account for about one-quarter of all mortgage applications—may encounter significant processing delays due to agency furloughs.” – Selma Hepp, Chief Economist at Cotality

- “By recent estimates, more than 2,500 mortgage originations per working day are at risk of delays during a shutdown . . .” – Zillow

- Flood insurance approvals may also be paused. The National Flood Insurance Program can be temporarily affected, which delays closings in flood zones.

Even with those challenges and delays, most transactions still go through. Buyers keep buying, sellers keep selling, and agents keep helping people move forward.

The Housing Market Usually Bounces Back Fast

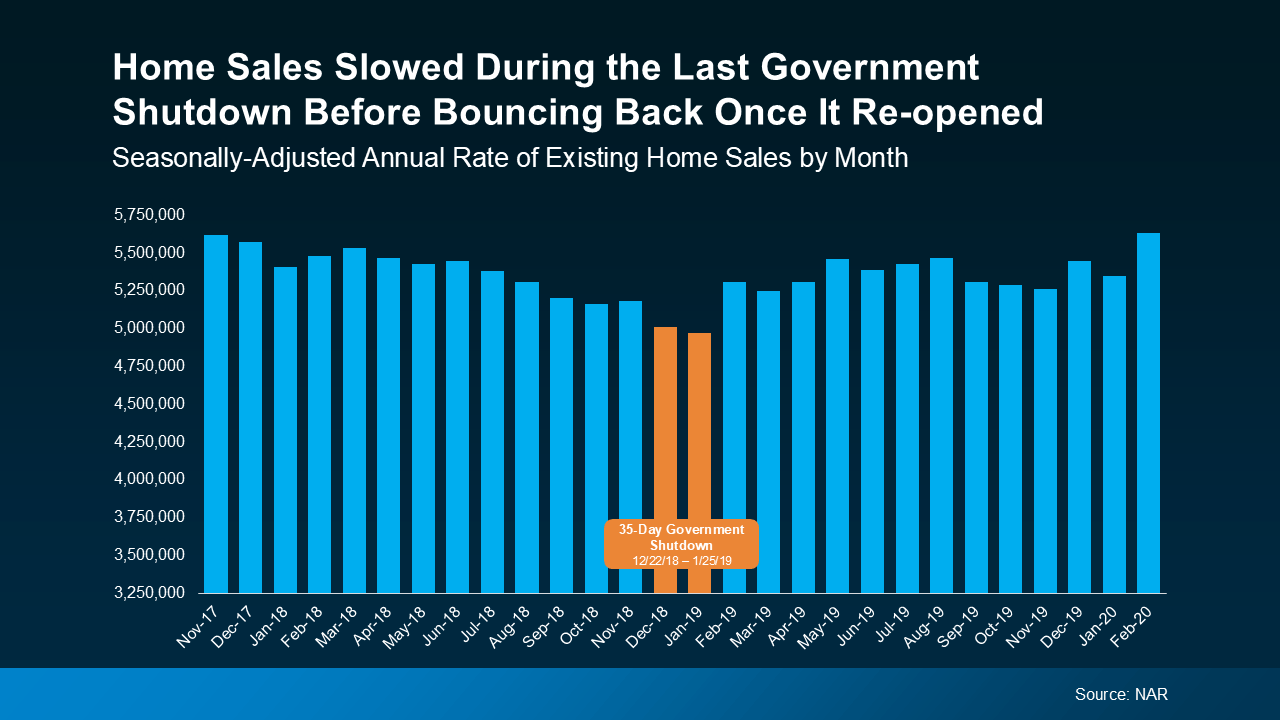

And you can see that play out in this data. If you look back at the most recent government shutdown that began at the end of 2018 and lasted for 35 days, sales activity dipped very slightly during the closure but picked right back up once the government reopened.

Data from the National Association of Realtors (NAR) shows existing home sales slowed for about two months, and then rebounded quickly as delayed closings worked their way through the system when the government reopened (see graph below):

What’s important to note is that the slowdown you see in the orange bars on this graph wasn’t simply due to seasonality in a typical housing market cycle. The sharper, shorter drop in this case lines up exactly with the 35-day government shutdown, and then sales bounced back as soon as it ended.

What’s important to note is that the slowdown you see in the orange bars on this graph wasn’t simply due to seasonality in a typical housing market cycle. The sharper, shorter drop in this case lines up exactly with the 35-day government shutdown, and then sales bounced back as soon as it ended.

What This Means for You

If you’re in the middle of buying or selling a home, don’t panic. Most deals will still move forward, even if it takes a few extra days. Jeff Ostrowski, Housing Market Analyst at Bankrate, explains:

“If you’re expecting to close in a week or a month, there could be some slight delay, but I think for most people, it’s probably going to be a blip more than a real deal killer.”

And if you’re just starting to think about buying or selling, this could actually work in your favor. Some buyers and sellers may become cautious and pause their plans during times of uncertainty, like this, and that can open a short window of opportunity.

When fewer people are active in the market, well-prepared buyers may find less competition for homes, and motivated sellers may be more willing to negotiate. These brief slowdowns often create a moment where you can make a move that would be harder once activity ramps back up.

Bottom Line

A government shutdown can cause short-term delays for some buyers, but it doesn’t derail the housing market. The last time this happened, sales picked back up as soon as the government re-opened.

If you’re unsure how this might affect your plans, or just want to make sense of what’s happening, connect with a local real estate agent.

If you’ve seen headlines or social posts calling for a housing crash, it’s easy to wonder if home values are about to take a hit. But here’s the simple truth.

The data doesn’t point to a crash. It points to slow, continued growth.

And sure, it’s going to vary by local area. Some markets will see prices rise more than others. And some may even see small, short-term declines. But the big picture is: home prices are expected to rise nationally, not fall, over the next 5 years.

The Real Story Is in the Expert Forecasts

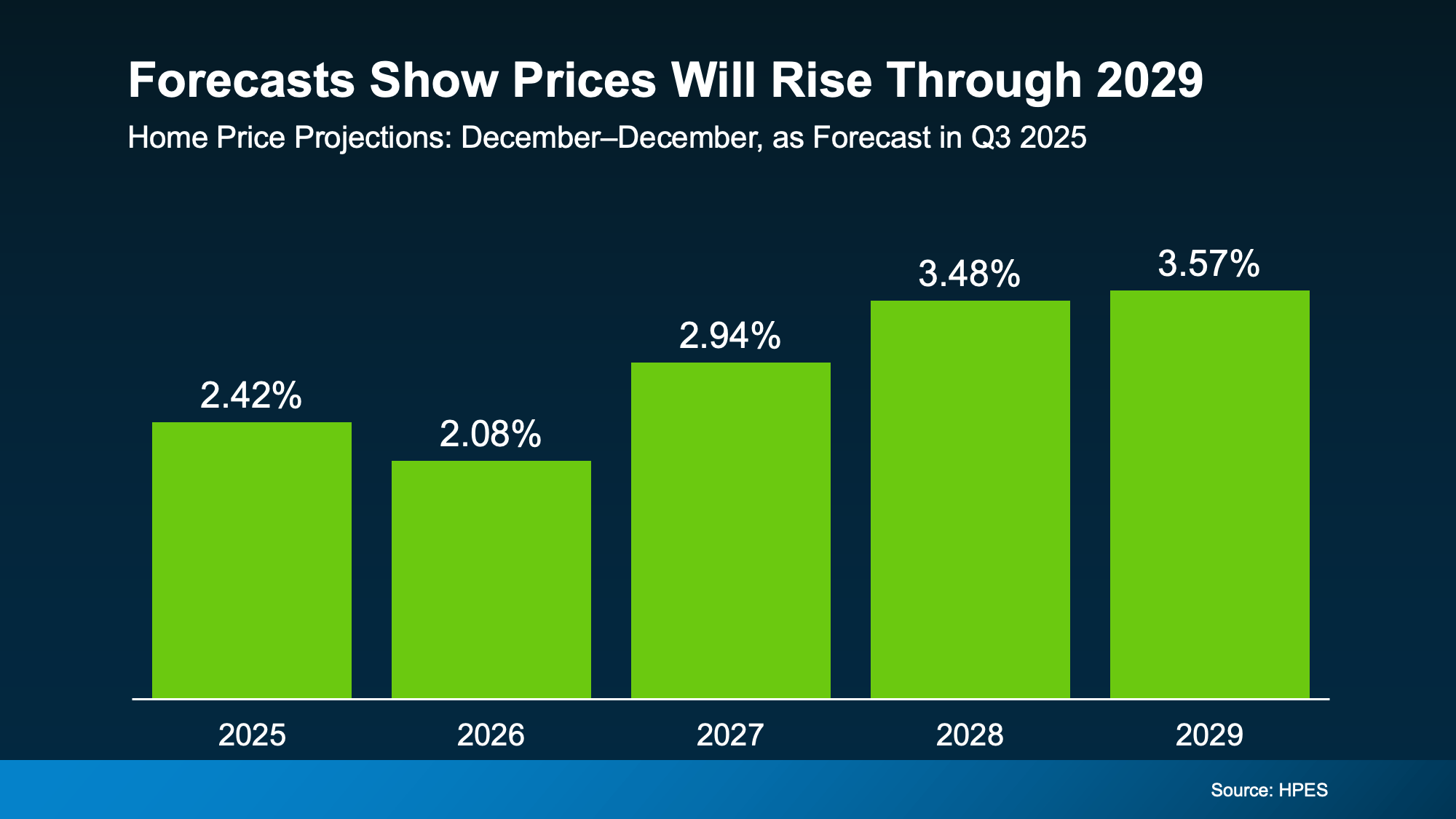

In the Home Price Expectations Survey (HPES) from Fannie Mae, each quarter over 100 leading housing market experts weigh in on where they project home prices will go from here. And in the report that was just released, the experts agree prices are projected to climb nationally through at least 2029 (see graph below):

Here’s how to read this visual. Each bar in that graph shows an increase, not a loss. It’s just that the anticipated pace of that appreciation varies year-to-year.

Here’s how to read this visual. Each bar in that graph shows an increase, not a loss. It’s just that the anticipated pace of that appreciation varies year-to-year.

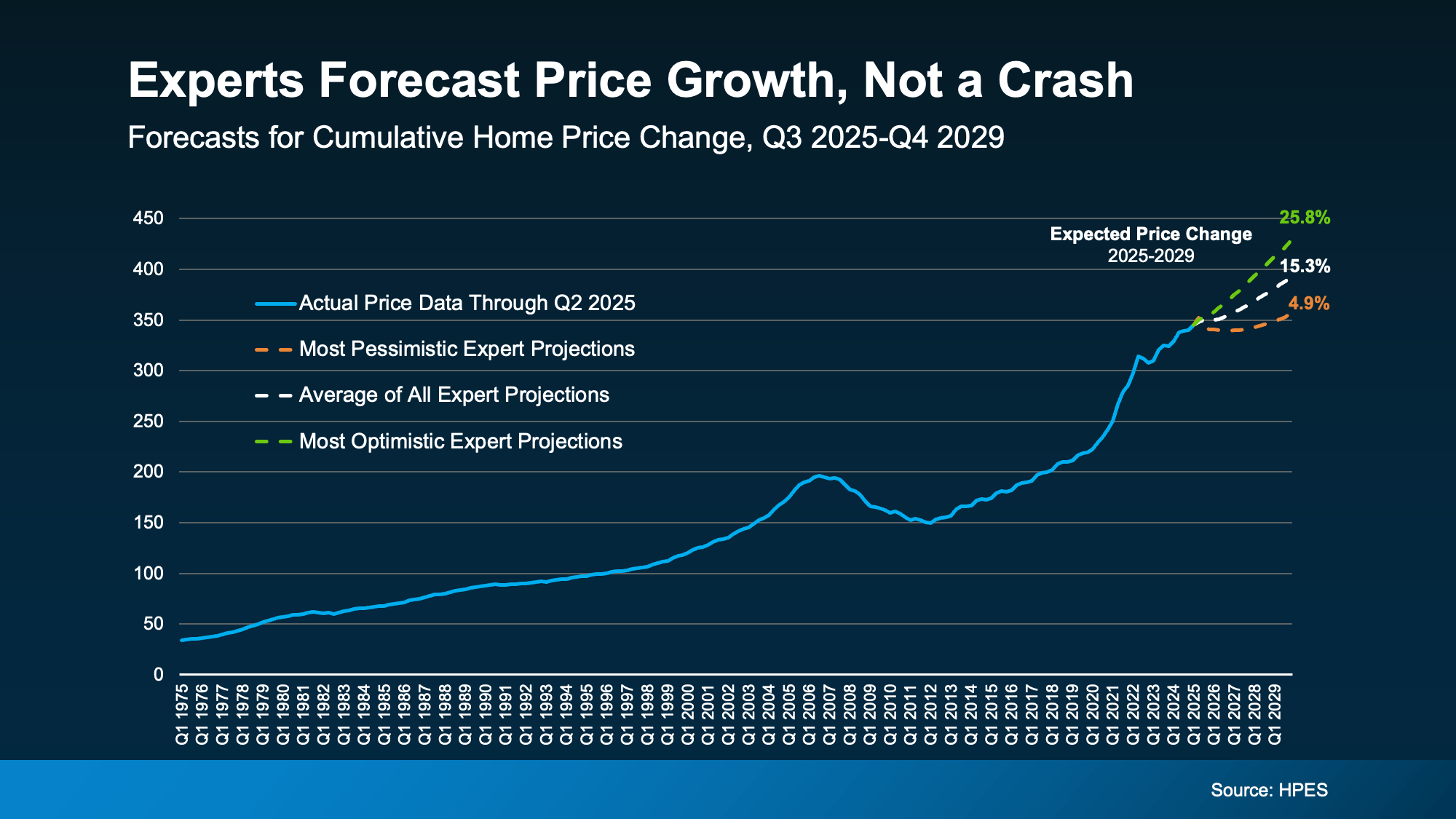

And to further drive this home, let’s look at another view of where prices are and where they’re expected to go. In this version, the expert forecasts are broken into 3 categories: the overall average, the most optimistic projections, and the most pessimistic projections (see chart below):

Notice how even the most pessimistic forecasters say we’ll see prices rise by almost 5% over the next few years.

Notice how even the most pessimistic forecasters say we’ll see prices rise by almost 5% over the next few years.

- Overall, prices are expected to rise about 15% from now through the end of 2029.

- The optimists say we’ll beat that and see a roughly 26% increase.

- And even the pessimists anticipate prices will go up by 5% during that period.

What sticks out the most? None of these groups who study the market are forecasting a crash, or even a decline, over the next 5 years.

How This Compares to “Normal” for the Market

Now, focus back on the first graph. The projections call for 2-3.5% price increases in each of the next five years. For context, the average rate of appreciation for the last 25 years was closer to 4-5% annually.

So, while that’s slightly below the historical average, it’s much more sustainable and typical than where the market was in 2020, 2021, and 2022.

Back then, prices rose too much, too fast based on record-low supply and record-high demand. Some places even saw prices climb by 15-20%.

So, while it may feel like prices are stalling compared to those pandemic-era surges, what’s really happening is that the market is finally finding balance again.

Why Prices Aren’t Expected To Crash

A lot of the chatter about home prices today is based on that rapid rise and the old saying that what goes up, must come down. But historically, that’s not really true. Home prices almost always rise.

And the main reason we’re not heading for a repeat of 2008 is simple: supply and demand.

Even though affordability challenges have made it harder for some people to buy over the past few years, there still aren’t enough homes for everyone who wants one. And that ongoing shortage is keeping upward pressure on prices nationally.

That’s why experts across the board can confidently agree: we’re not headed for a price collapse, but for steady, long-term appreciation.

And just in case it’s the economy that’s got you worried, remember this. Over the past 50 years, there have been plenty of economic events that have impacted the market. And one thing that’s consistently been true throughout time is the housing market always recovers. And we’re coming through that turn right now and going into a recovery.

Bottom Line

If you’ve been waiting to buy or sell because you’re worried about a crash, it’s time to look at the data – not the headlines.

The question isn’t if home prices will rise, it’s by how much.

Connect with an agent who can show you what’s happening in your local market and what these forecasts mean for your next move.

You Can’t Control What’s Happening with Mortgage Rates. But You Can Control This.

The Remodel You’ve Been Dreaming About May Be Closer Than You Think

Affordability Has Improved in All 50 States

-

Affordability4 weeks ago

Affordability4 weeks agoRenting vs. Buying: The Numbers Might Surprise You

-

For Sellers4 weeks ago

For Sellers4 weeks agoTop Mistakes Homeowners Are Making in 2026 (And How To Avoid Them)

-

For Sellers3 weeks ago

For Sellers3 weeks agoSpring Sellers Have an Edge. Here’s Why.

-

Downsize3 weeks ago

Downsize3 weeks agoThe Hidden Advantage Repeat Buyers Have Right Now

-

Equity3 weeks ago

Equity3 weeks agoAre Home Prices Dropping? Here’s the Real Story.

-

Agent Value2 weeks ago

Agent Value2 weeks agoIf Your House Isn’t Getting Offers, Read This.

-

Affordability2 weeks ago

Affordability2 weeks agoShould You Wait for Lower Rates?

-

For Buyers2 weeks ago

For Buyers2 weeks agoOne Key Sign We’re Not Headed for a Wave of Foreclosures

You must be logged in to post a comment Login