Buying Tips

Thought the Market Passed You By? Think Again.

If you stepped back from your home search over the past few years, you’re not alone – and you’re definitely not out of options. In fact, now might be the ideal time to take another look. With more homes to choose from, prices leveling off in many areas, and mortgage rates easing, today’s market is offering something you haven’t had in a while: options.

Experts agree, buyers are in a better spot right now than they’ve been in quite a long time. Here’s what they have to say.

Affordability Is Finally Improving

Lisa Sturtevant, Chief Economist at Bright MLS, says affordability is finally starting to turn the corner:

“Slower price growth coupled with a slight drop in mortgage rates will improve affordability and create a window for some buyers to get into the market.”

Mortgage rates have eased from their recent highs, price growth has slowed, and that one-two combo is making homes more affordable than they’ve been in months.

There Are More Homes on The Market

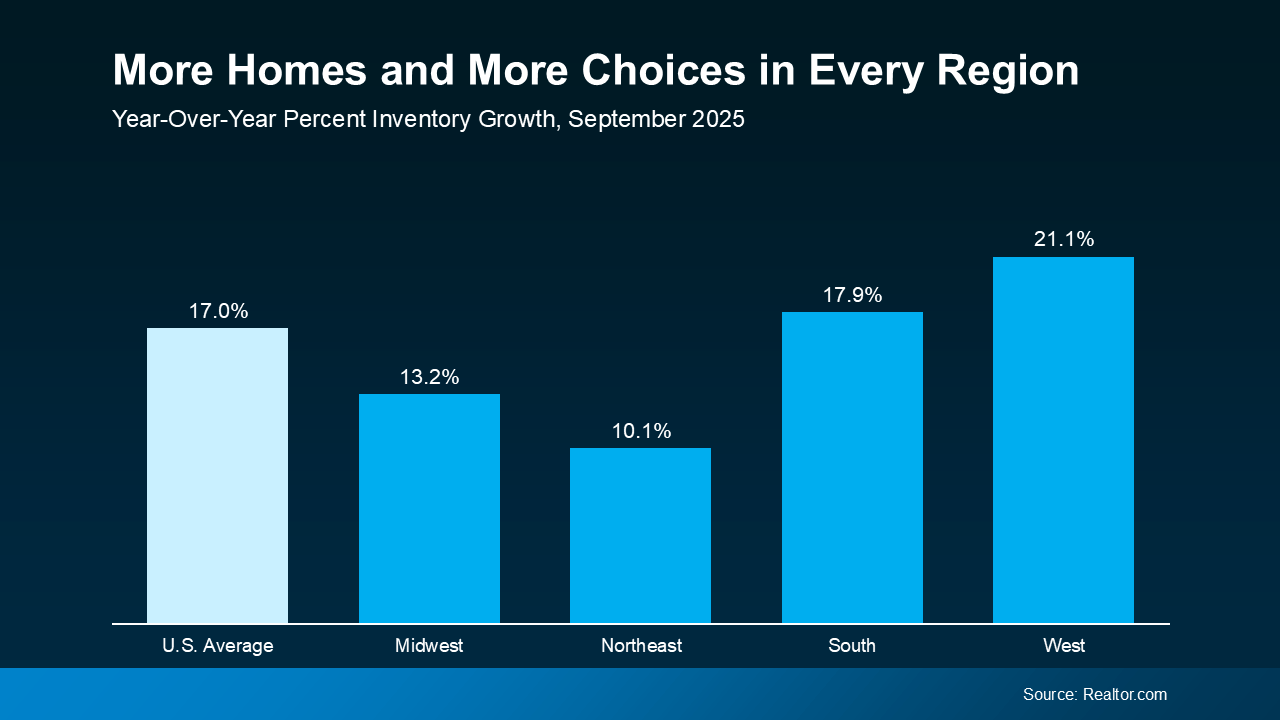

And a big reason prices are easing is because there are more homes on the market. According to the latest from Realtor.com, there are 17% more homes for sale today than there were at this time last year. That means more options, less competition with other buyers, and a chance to find the space that actually works for you.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), shares:

“Homebuyers are in the best position in more than five years to find the right home and negotiate for a better price. Current inventory is at its highest since May 2020, during the COVID lockdown.”

Take a look at the numbers.

As Yun notes, inventory is up everywhere. Compared to this time last year, every region of the country has more homes on the market than at this time last year (see graph below):

That translates to more homes to choose from, whether you’re looking for a bigger backyard, a shorter commute, or finally ditching your rental.

That translates to more homes to choose from, whether you’re looking for a bigger backyard, a shorter commute, or finally ditching your rental.

But not all markets are the same…

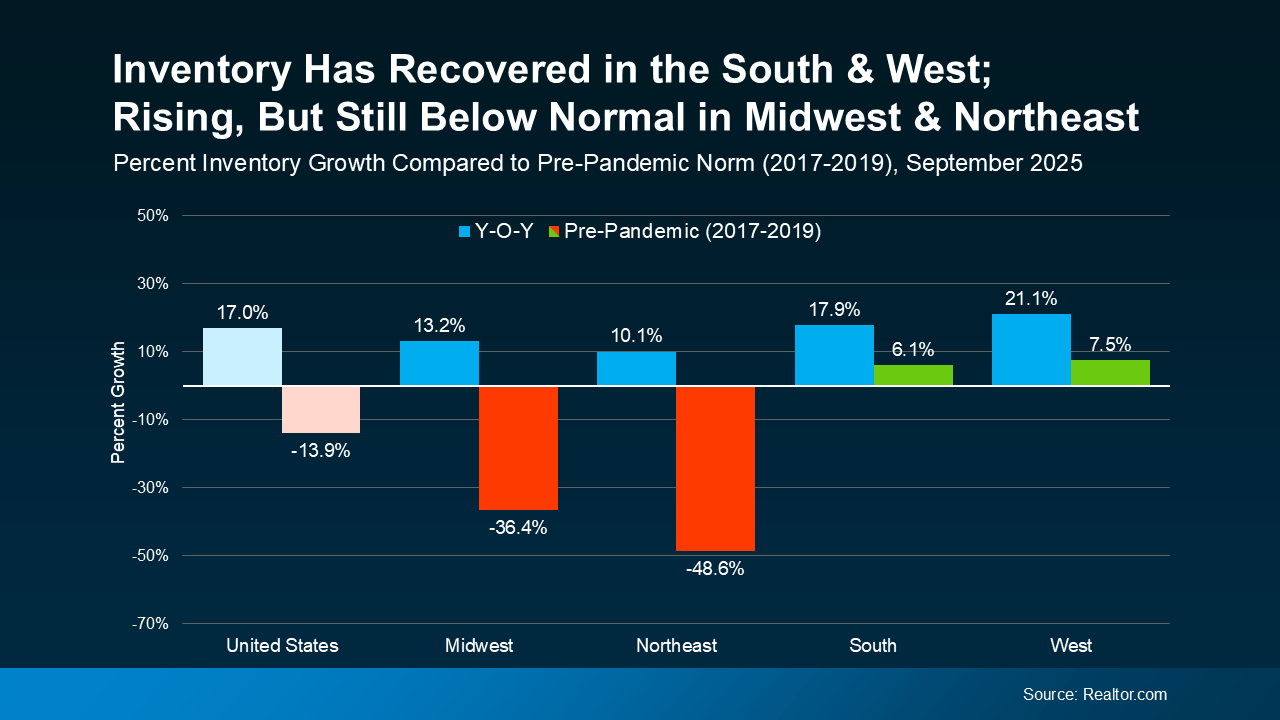

When you compare current inventory growth to pre-pandemic norms (2017–2019), the picture changes a bit, depending on where you are (see graph below):

The green bars show where inventory has fully recovered (and even grown above pre-pandemic levels) in the South and the West. Supply, however, is still tighter in the Northeast and Midwest, as shown in the red bars, where inventory is still below normal.

The green bars show where inventory has fully recovered (and even grown above pre-pandemic levels) in the South and the West. Supply, however, is still tighter in the Northeast and Midwest, as shown in the red bars, where inventory is still below normal.

And here’s why that’s still a win everywhere.

When you step back and look at the bigger picture, with inventory up in every region, that means more choices everywhere, even if some areas have more homes for sale than others.

And with fewer buyers in the market and more homes for sale, sellers are willing to negotiate to get a deal done.

All of that adds up to a win for today’s buyers.

And it’s also why working with a local expert really makes a difference. What’s happening in your zip code or neighborhood might look different than the national or regional trend. But the overall takeaway is clear: with more homes on the market, buyers have more leverage than they did a year or more ago.

So, if you stepped away from your search because things felt too competitive, too pricey, you were worried about finding a home, or it was all just too much to process, this could be your moment to take another look.

And if you’re not quite ready to go all in, that’s okay too. You can start by planning ahead. That means working with a trusted agent who can help you break down your budget, narrow your search, and make sure you’re prepped and ready when the right home hits the market.

Bottom Line

Want to know what’s happening in your local market? Reach out to a trusted real estate agent and ask for a custom overview of what’s available right now, so you can learn how to be ready when the timing is right for you.

Because this isn’t 2021.

This isn’t even 2023 or 2024.

This is a new market – and you might be surprised by what you find.

Mortgage rates have been volatile lately. And if you’re thinking about buying a home, that can make it harder to plan. But there are still things you can do to get the best rate possible in today’s market. It starts with having the right information.

So, what’s causing the bumps in rates? And what can you do about it? Let’s break it down.

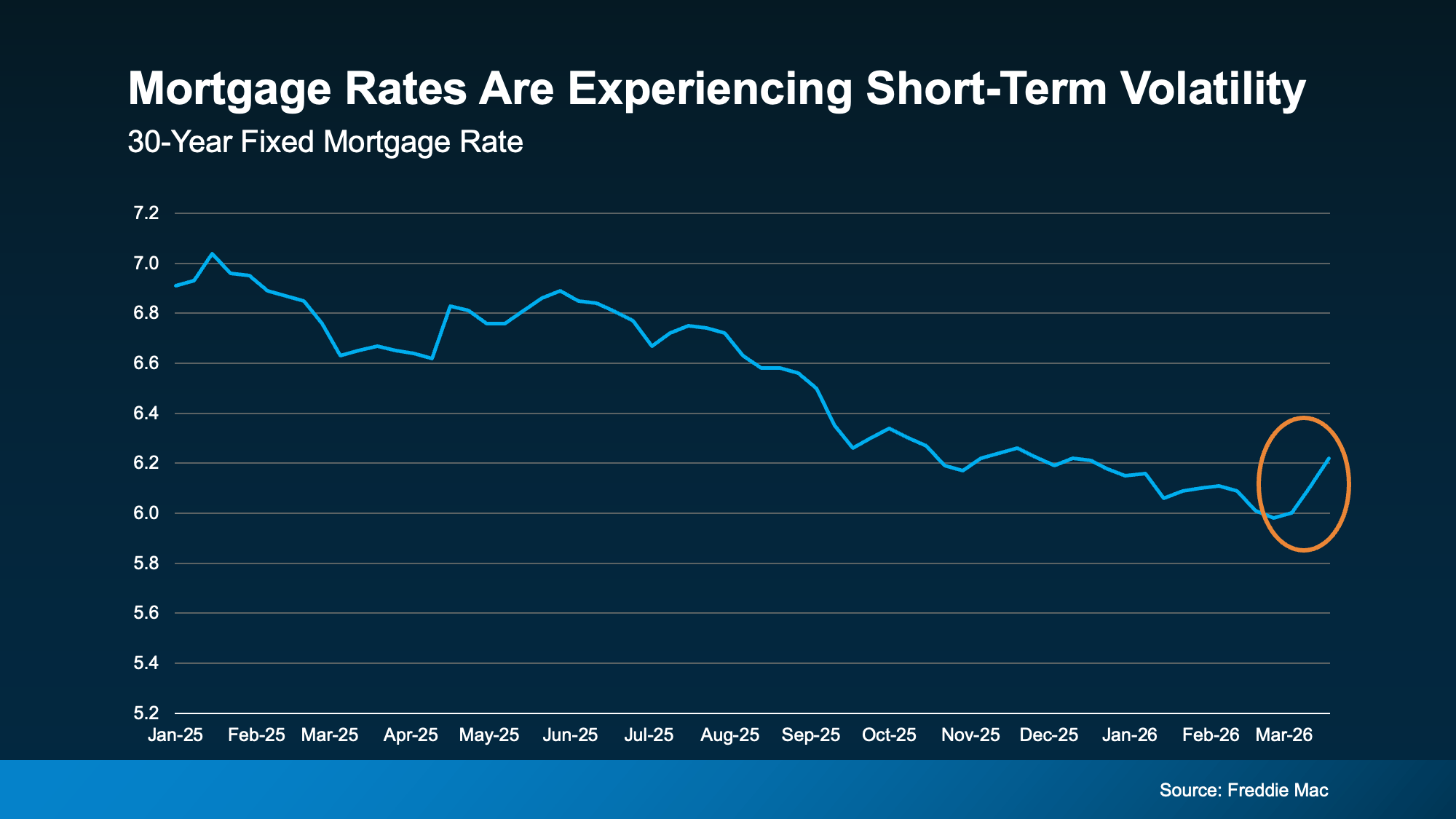

Mortgage Rate Volatility Is Normal

Data from Freddie Mac shows the recent volatility. After trending down for well over a year, there was a rise this month (see graph below):

While it’s easy to be distracted by the changes, here’s what you need to remember.

It’s normal for rates to bounce around a bit here and there. For example, if you look back at the graph, you’ll see that even within the past year there have been times like this when rates inched up. We’re in one of those moments right now and you need to be aware of that.

Especially when there’s economic uncertainty or big global events happening, volatility like this is expected. As Investopedia explains:

“Mortgage rates don’t move in isolation. When global events inject uncertainty into financial markets . . . that can ripple through to borrowing . . . mortgage costs can respond quickly to geopolitical developments. As long as uncertainty remains elevated, rate swings may continue.”

And that’s one of the reasons why trying to time the market isn’t a wise move.

You can’t control what happens with mortgage rates. But there are still things you can do to help you get the best rate possible in today’s market. And here’s where to focus your effort.

Your Credit Score

Your credit score plays a big role in the rate you qualify for. Even a small improvement can make a noticeable difference in your monthly payment. As Bankrate puts it:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

So, make sure you do what you can to keep your credit score up. If you’re not sure what your score is or how you can improve it, talk to a trusted loan officer.

Your Loan Type

There are also different types of home loans – and each one can have unique requirements, benefits, and rates for qualified buyers. The Consumer Financial Protection Bureau (CFPB) explains:

“There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans. Lenders decide which products to offer, and loan types have different eligibility requirements. Rates can be significantly different depending on what loan type you choose.”

That’s why it’s so important to explore your options with a lender. You may even want to talk to multiple lenders to see how the options vary.

Your Loan Term

The length of your loan matters too. Most lenders typically offer 15, 20, or 30-year loans. Freddie Mac offers this advice:

“When choosing the right home loan for you, it’s important to consider the loan term, which is the length of time it will take you to repay your loan before you fully own your home. Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

Again, to figure out what makes the most sense for your budget and long-term goals, have a lender walk you through all your options.

Bottom Line

Thinking about buying right now? The best advice is to accept that you can’t control where rates are going to go from here.

What you can do is work with a trusted lender and take steps that’ll help you get the best rate possible.

So, if you want to move today, talk to an agent and a lender to make it happen. You just need to control the controllables and focus where it counts.

Your House Hasn’t Sold Yet. Should You Rent It Out Instead?

Before You Fall in Love with a House, Do This First.

Don’t Let Home Prices Headlines Fool You

-

Agent Value4 weeks ago

Agent Value4 weeks agoIf Your House Isn’t Getting Offers, Read This.

-

Affordability4 weeks ago

Affordability4 weeks agoShould You Wait for Lower Rates?

-

For Buyers4 weeks ago

For Buyers4 weeks agoOne Key Sign We’re Not Headed for a Wave of Foreclosures

-

Agent Value3 weeks ago

Agent Value3 weeks agoThe #1 Reason Buyers Walk Away (And How To Get Ahead of It)

-

For Buyers7 days ago

For Buyers7 days agoDon’t Let Home Prices Headlines Fool You

-

Affordability3 weeks ago

Affordability3 weeks agoAffordability Has Improved in All 50 States

-

Agent Value3 weeks ago

Agent Value3 weeks ago3 Must-Do’s for First-Time Home Buyers

-

Equity2 weeks ago

Equity2 weeks agoThe Remodel You’ve Been Dreaming About May Be Closer Than You Think

You must be logged in to post a comment Login