Forecasts

How To Buy a Home Without Waiting for Lower Rates

Many people are hoping mortgage rates will come down before they buy a home. But will that actually happen? According to the latest forecasts, experts say rates will decline, but not by as much as a lot of people want.

The good news? Even if they don’t drop substantially, there are still ways to make buying a home more affordable.

How Much Will Rates Drop?

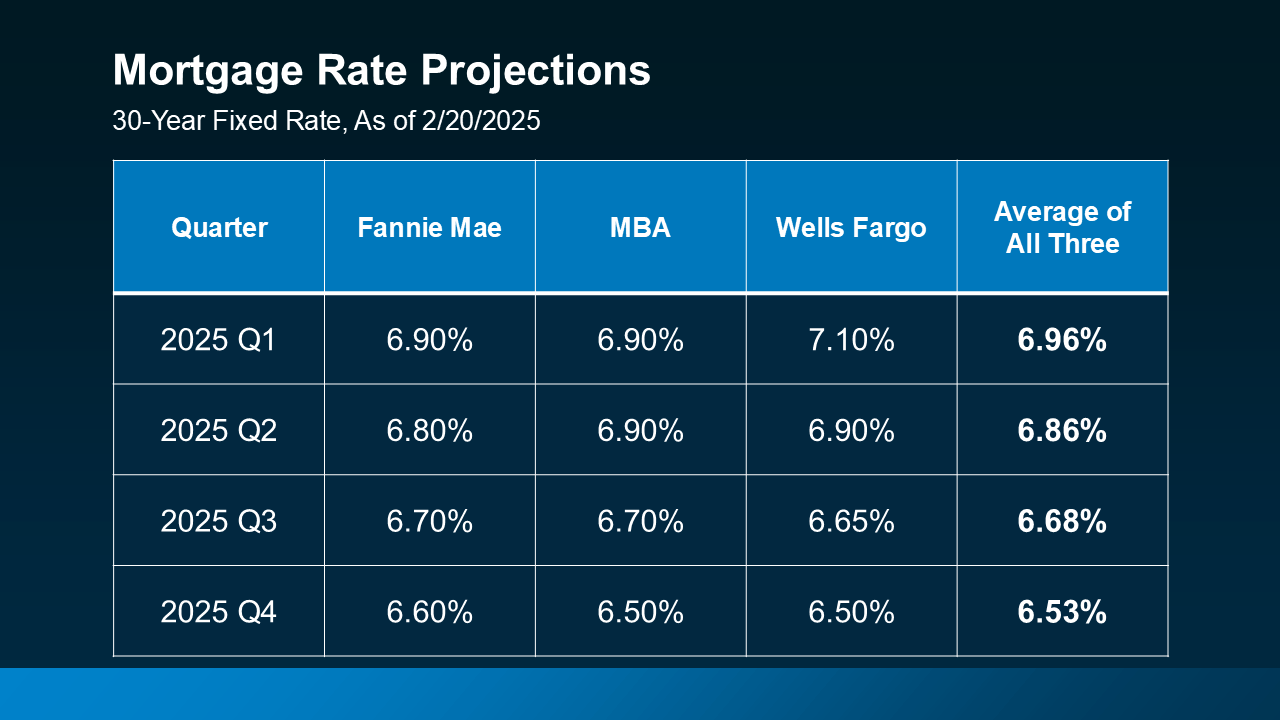

A few months ago, experts were forecasting mortgage rates could dip below 6% by the end of the year. But recent projections suggest that may not happen after all.

While mortgage rates are still expected to decline some later this year, projections from Fannie Mae, the Mortgage Bankers Association (MBA), and Wells Fargo now show them stabilizing closer to the 6.5% to 7% range (see below):

That means if you’re holding off on buying a home in hopes of much lower mortgage rates, you may be waiting a while. And if you need to move because something in your life has changed, like a new job, a new baby, or a marriage – waiting that long may not be an option.

That means if you’re holding off on buying a home in hopes of much lower mortgage rates, you may be waiting a while. And if you need to move because something in your life has changed, like a new job, a new baby, or a marriage – waiting that long may not be an option.

Creative Financing Options in Today’s Market

Since rates aren’t expected to decline as much as originally expected, it may be worth considering alternative financing options that could help you get into a home sooner rather than later. Here are three strategies to discuss with your lender to see if any of these make sense for you:

1. Mortgage Buydowns

A mortgage buydown allows you to pay an upfront fee to lower your mortgage rate for a set period of time. This can be especially helpful if you want or need a lower monthly payment early on. In fact, 27% of agents say first-time homebuyers are increasingly requesting buydowns from sellers in order to buy a home right now.

2. Adjustable-Rate Mortgages

Adjustable-rate mortgages (ARMs) typically start with a lower mortgage rate than a traditional 30-year fixed mortgage. This makes them an attractive option, especially if you expect rates to drop in the coming years or plan to refinance later.

And if you remember the housing crash, know that today’s ARMs aren’t like the risky ones back then. Lance Lambert, Co-Founder of ResiClub, helps drive this point home by saying:

“. . . ARM products today are different from many of the products issued in the mid-2000s. Before 2008, lenders often approved ARMs based on borrowers ability to pay the initial lower interest rates. And sometimes they didn’t even check that (remember Ninja loans). Today, adjustable-rate borrowers qualify based on their ability to cover a higher monthly payment, not just the initial lower payment.”

In simple terms, banks used to give loans without checking to see if buyers could afford them. Now, lenders verify income, assets, and jobs, reducing the risks associated with ARMs compared to the past.

3. Assumable Mortgages

An assumable mortgage allows you to take over the seller’s existing loan — including its lower mortgage rate. And with more than 11 million homes qualifying for this option according to U.S. News, it’s worth exploring if you want or need a better rate.

Bottom Line

Waiting for a big decline in mortgage rates may not be the best strategy. Instead, options like buydowns, ARMs, or assumable mortgages could make homeownership more affordable right now. Connect with a local lender to explore what works for you.

How does this impact your homebuying plans this year?

If the housing market feels confusing right now, you’re not alone.

Mortgage rates have risen. Home sales haven’t picked up like expected. And many buyers and sellers are wondering when things are going to feel easier or be more affordable.

The truth is: a lot changed over the first half of this year.

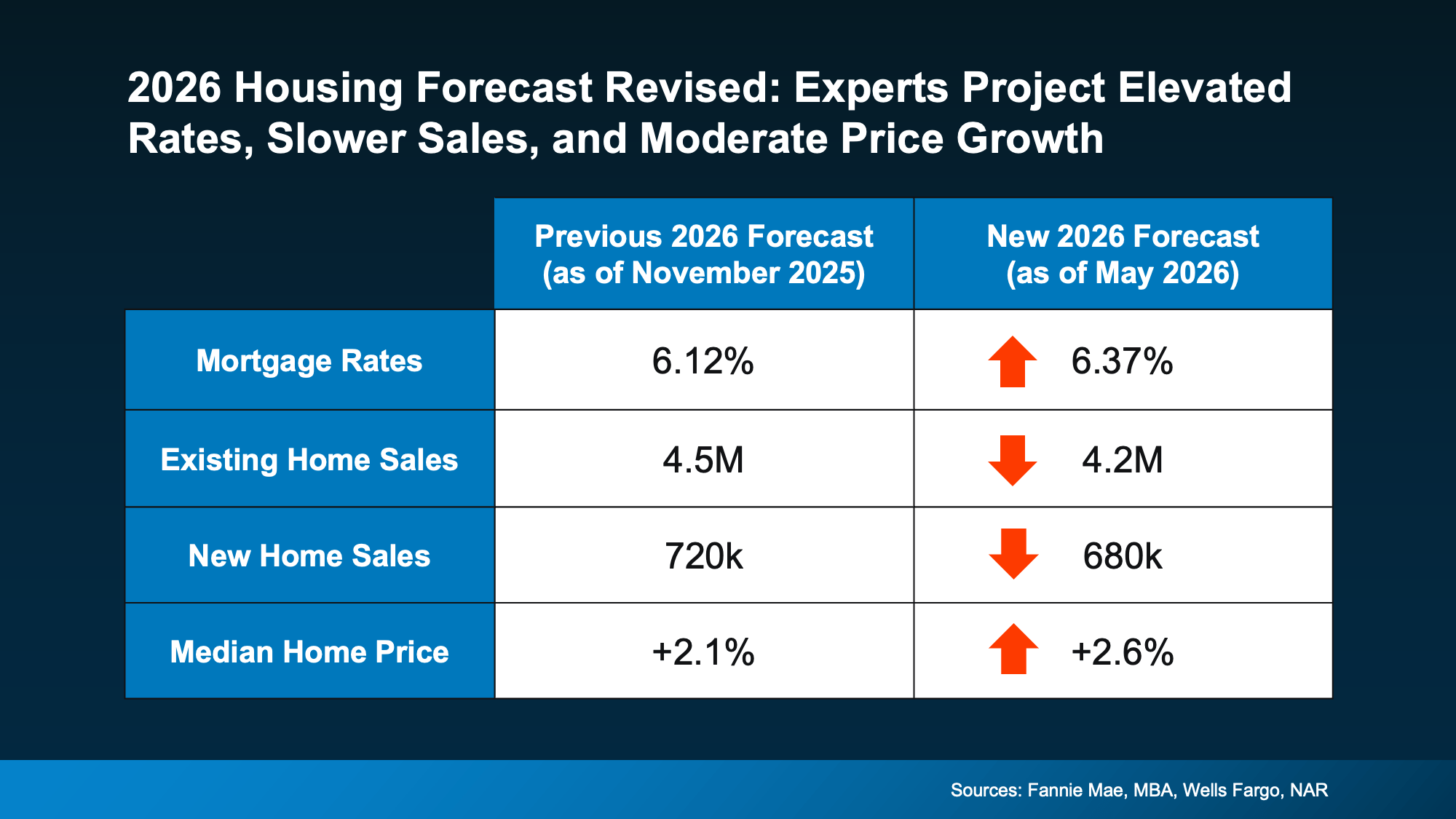

Back at the end of 2025, economists were forecasting a much stronger housing market for 2026. They expected mortgage rates to come down, affordability to improve more dramatically, and home sales to rebound.

But lingering inflation, economic uncertainty, and growing geopolitical tensions overseas pushed mortgage rates higher than expected. And because rates stayed elevated for longer, many buyers continued to hold off.

That’s why experts recently revised their housing forecasts for the rest of the year (see graph below):

So, what does this actually mean for you? Let’s break it down.

Mortgage Rates May Remain Elevated

While just about everyone wants mortgage rates to go back to the uppers 5s or low 6s we saw at the start of the year, as of right now, the experts don’t think that’s likely to happen this year.

Instead, forecasts have been updated from the low 6s they originally projected. Many industry organizations are saying rates will stay in roughly the mid 6s this year. The good news is, that’s still lower than rates were a year ago.

Of course, this is based on what we know today. If the conflict overseas comes to an end or inflation drops, this could change. But if you’re waiting for lower rates, it may not pay off in the way you expect.

Existing Home Sales Revised Lower

Back in late 2025, experts expected we’d sell an average of 4.5 million homes this year. Now? That’s dropped down a bit to 4.2 million.

That tells us something important: buyers are still hesitant because affordability remains challenging.

Higher mortgage rates have made monthly payments harder to manage, especially for first-time buyers. And that’s slowed the pace of the market compared to what was originally expected. But even though the forecast was revised down, we’re still expected to sell more homes than last year.

Once geopolitical tensions resolve and rates begin to settle down, many experts believe that group of buyers will be ready to jump back in. As Lawrence Yun, Chief Economist at NAR, explains:

“There is sizable pent-up demand that could be released into the market.”

There has already been a few glimmers of renewed hope lately. In recent months, pending homes sale have been improving month-over-month despite higher rates.

So, if you’re able to afford a home at today’s rates, it could still make sense to buy now. Because otherwise, if you wait, you’ll have more competition (and potentially fewer homes to choose from) when those others buyers jump back in.

New Home Sales Also Slowed

Builders also expected to have a stronger year. Earlier forecasts projected new home sales would top 700k in 2026. Now, economists expect we’ll be just shy of that number.

Again, mortgage rates are a major reason why.

But the upside for buyers is that builders may be even more motivated to sell. That means builder incentives, negotiation opportunities, and pricing flexibility may continue in many markets. So, if you live somewhere where there’s more new construction, this may actually be a bright spot for you.

Builders could be more ready to negotiate, and that gives you more leverage to get a better deal.

Home Prices Are Still Expected To Rise

This is one of the most important takeaways from the entire forecast. Even though sales activity is slower, on average, experts did not revise their home price forecast downward.

They still expect prices to rise nationally this year.

Why? Because while buyer demand has softened, the number of homes for sale is still relatively limited overall. That imbalance is helping support prices, even in a slower market.

Of course, conditions vary depending on where you live. Some markets are cooling more than others. But nationally, experts are still projecting steady price growth — not a major decline. And that should be a comfort whether you’re buying or selling.

Because sellers don’t want a major drop in prices. And while buyers may think they do, generally you feel better about a big purchase when it doesn’t depreciate right away.

Bottom Line

The housing market hasn’t rebounded as quickly as experts originally hoped. But that doesn’t mean it’s stalled.

Higher inflation and lingering economic uncertainty caused economists to revise their forecasts for this year. But importantly, when those two things settle down, many experts believe the market will regain its momentum.

So don’t see this revision in forecasts as a sign of trouble. See it as a temporary reaction to overall conditions and uncertainty.

If you want to know what’s happening in your local market, and what it could mean for your plans for the rest of this year, talk to a local agent.

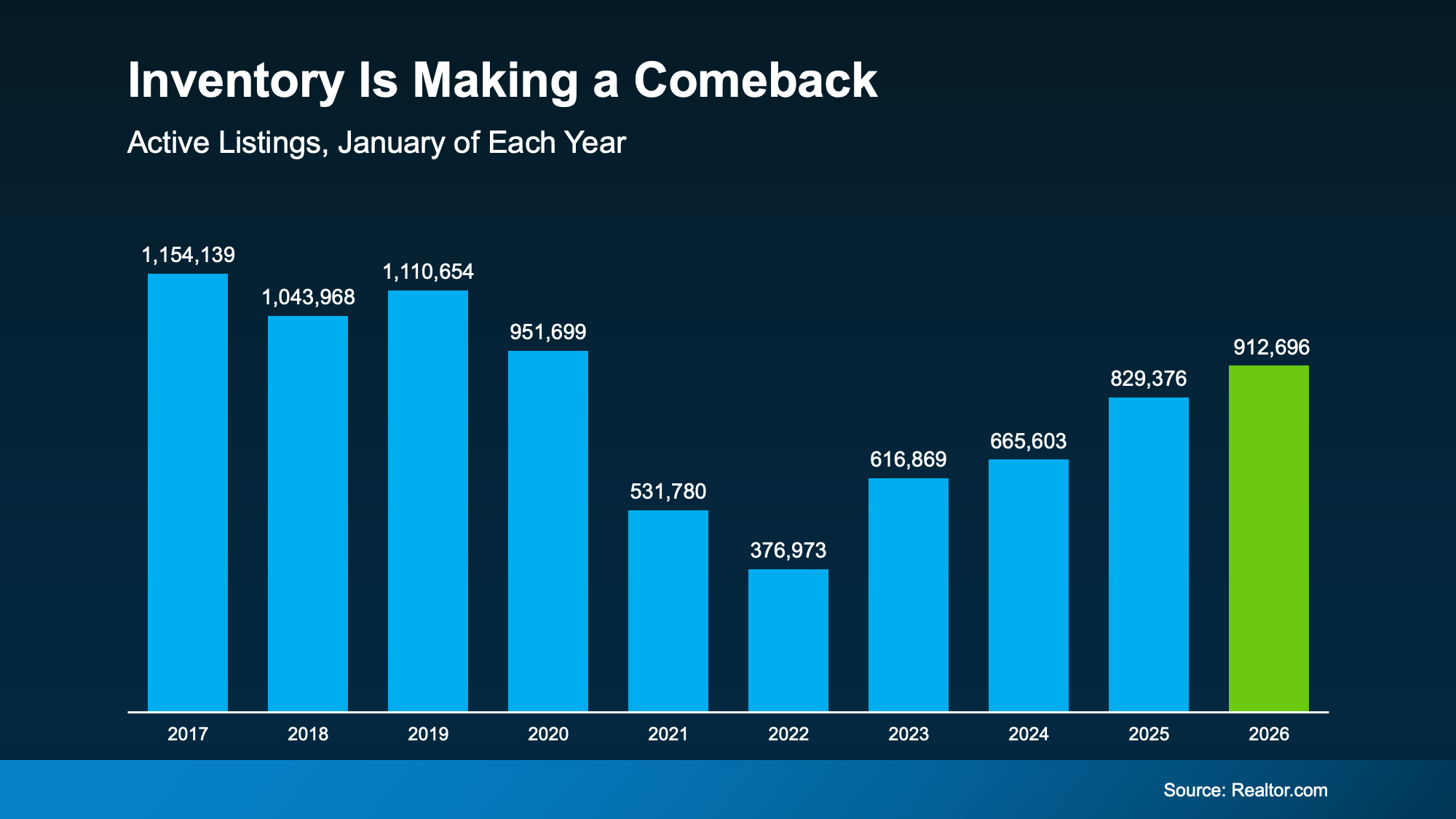

After a long stretch where buyers were competing for too few homes, inventory has made a comeback over the past year. And depending on where you live, that’s opening up your options in a meaningful way.

According to Realtor.com, the number of homes available for sale in January was the highest it’s been since 2020. Here’s why that’s such a big deal. Getting back to pre-pandemic levels signals a slow and steady return to what’s typical:

Now, it’s worth noting, nationally we’re not there yet – and having more inventory improving won’t suddenly “fix” the market. But the growth we’ve seen lately still changes how competitive the market feels.

Now, it’s worth noting, nationally we’re not there yet – and having more inventory improving won’t suddenly “fix” the market. But the growth we’ve seen lately still changes how competitive the market feels.

- When there are more homes for sale, buyers gain time, options, and leverage.

- When there aren’t, the pressure ramps up quickly.

In the years since 2020, there weren’t enough homes for sale, and that made the market feel different. Rushed. Stressful. Intimidating.

But now it’s finally getting better.

A Growing Portion of the Country Is Getting Back to Normal

Depending on where you live, inventory growth is going to vary. Some places are bouncing back faster than others. According to Lance Lambert, Co-Founder of ResiClub, in January 2025, just a little over one year ago, only 41 of the 200 largest metros were back to normal inventory-wise.

But around the end of year, almost half (90) of the largest 200 metro areas were back at or above typical levels. That’s a big improvement in roughly a year. And it’s not done yet.

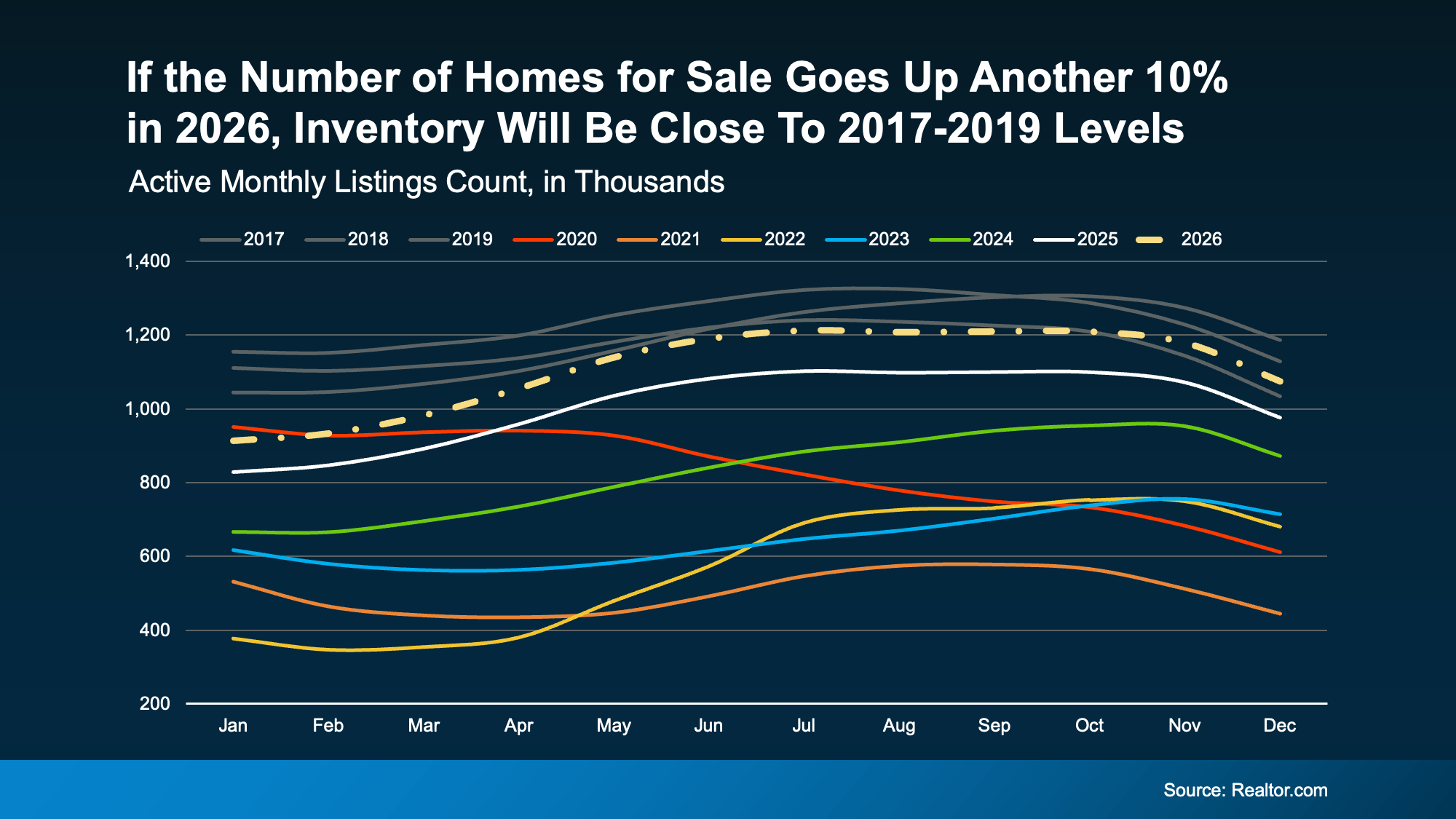

Inventory Is Expected To Keep Growing

Looking ahead, forecasts suggest the number of homes for sale could rise another 10% this year, which means even more markets should join the list of places where supply has rebounded.

Here’s a graph that shows what an extra 10% would do for the market this year. You can see that projected growth (shown in the dotted line) hits inventory levels seen in 2017-2019 by roughly this fall (the gray lines). That means we may reach normal by end of year, nationally:

And that changes your home search in a good way. As Hannah Jones, Senior Economic Research Analyst at Realtor.com, puts it:

“. . . housing market conditions are gradually rebalancing after several years of extreme seller advantage. Buyers are beginning to see more options and modest negotiating power as inventory improves . . .”

In other words, the market is starting to work with buyers again — not against them.

Bottom Line

Inventory isn’t fully back to normal everywhere. But it’s moving in the right direction. And, in some areas, it’s already there.

If you’ve been waiting for a moment when you have options and a little breathing room, this is the strongest setup buyers have seen in a long time.

If you want to know what’s happening in your local market, talk to an agent.

Who doesn’t love a top 10 list? Well, here are two top 10 lists for the housing market this year. But before you take a look, there’s something you should know.

If a move is on your radar for 2026, here’s the most important thing you need to understand upfront: there isn’t one housing market this year – there are many.

Experts agree 2026 is shaping up to be one of the most geographically split housing markets in years. Some areas are tilting in favor of sellers, while others are opening real doors for buyers. Who has the advantage depends almost entirely on where you are. Selma Hepp, Chief Economist at Cotality, puts it this way:

“Looking ahead to 2026, regional differences will remain pronounced, with demand favoring areas that offer both economic opportunity and relative affordability.”

To show just how divided the landscape is, here’s a look at where sellers are expected to have the upper hand, and where first-time buyers may finally find their opening this year.

Where Sellers Are Poised To Win Big in 2026

Zillow identified the following metros as some of the strongest seller markets for 2026, based on buyer demand, pricing momentum, and how quickly homes are expected to sell:

In markets like these, buyers are going to be competing for limited inventory, which gives sellers more leverage.

In markets like these, buyers are going to be competing for limited inventory, which gives sellers more leverage.

Homeowners in seller’s markets this year can expect:

-

Stronger buyer interest

-

Shorter time on market

-

Better odds of selling close to (or above) asking price

That doesn’t mean every listing is guaranteed success. But it does mean sellers who prepare well and lean on an agent’s expertise should be very happy with their results in 2026.

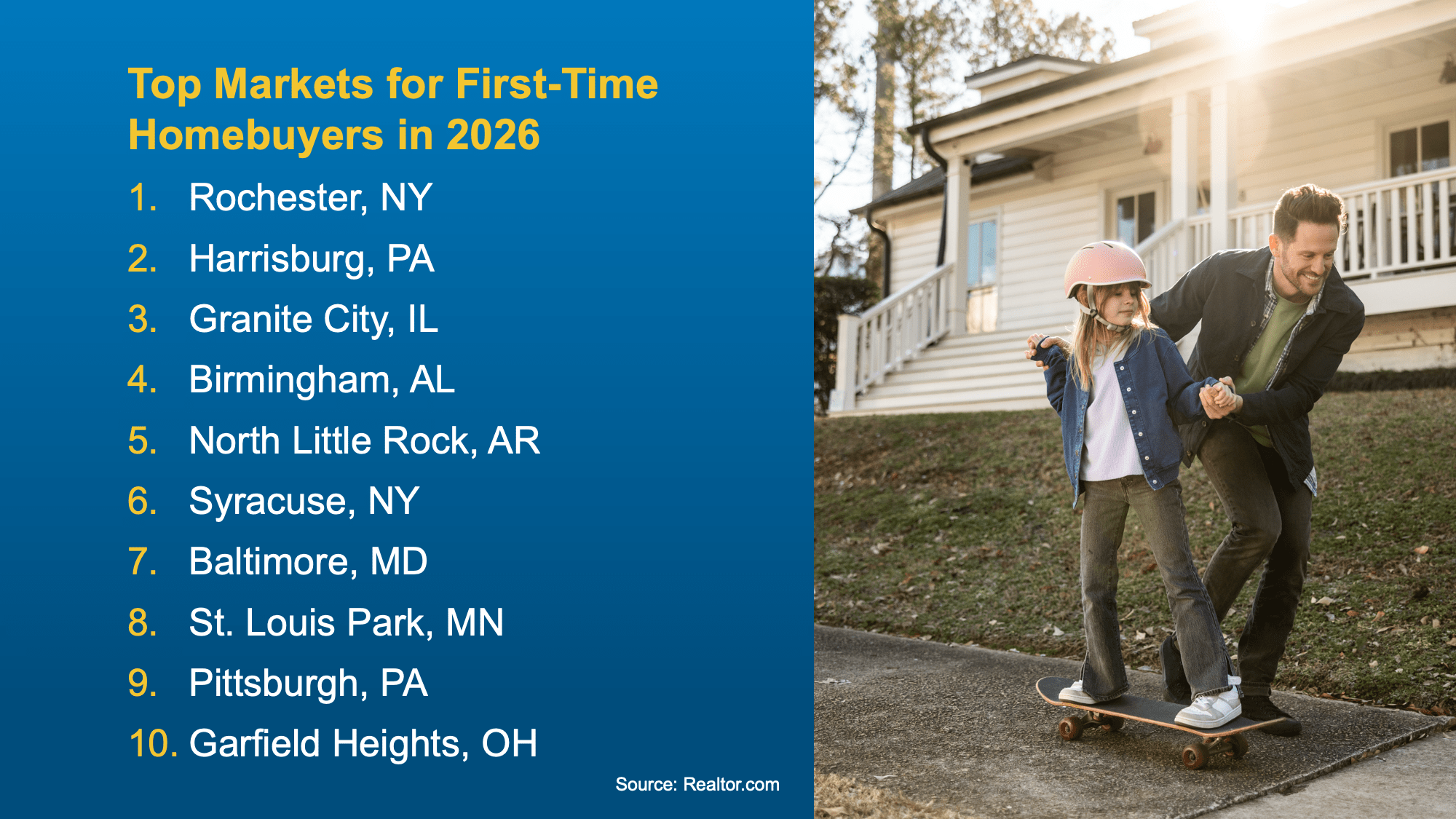

Markets Where There’s More Opportunity for First-Time Buyers

On the flip side, here’s a look at where buyers have the power – in particular, first-time buyers, since they’ve had the hardest time breaking into the market lately. Realtor.com highlights the top metros where first-time buyers are expected to have better opportunities in 2026:

These markets stand out for a mix of:

These markets stand out for a mix of:

-

More affordable home prices

-

Better housing availability

-

Strong local amenities and economic health

For first-time buyers, that combination matters. It’s what could finally turn “someday” into “this could actually work.” In buyer’s markets, they should expect:

-

Less intense competition

-

More room to negotiate

-

A clearer path to getting an offer accepted

What Matters More Than Any Top 10 List

Not seeing your city on the list? Don’t stress. This is just a national snapshot, not a judgment on your local market. The goal here is just to show you how different the market really is depending on where you are.

And remember, you can buy or sell no matter how your local market leans. You just need an agent’s help to figure out the right strategy to get it done. For example:

-

A seller in a more buyer-friendly metro may need to be aggressive on their price and prep.

-

A buyer in a seller-leaning area may still need to come prepared with their best offer.

To find out where your market falls and what you should expect, you’ll want the help of a local expert.

Bottom Line

The housing market in 2026 isn’t one-size-fits-all. It’s a year where local conditions matter more than ever.

Whether your market leans more buyer-friendly or seller-friendly, the right strategy can put you in a strong position. And that’s where a local expert comes in. Connect with a trusted real estate agent today.

Two Big Reasons To Move This Summer

Lower Asking Prices Are a Win for Today’s Buyers

Could Moving a Bit Further Out Change Everything About Your Budget?

-

Equity4 weeks ago

Equity4 weeks agoRecord High Mortgage Debt Sounds Scary. Here’s What the Headlines Leave Out.

-

Equity4 weeks ago

Equity4 weeks agoAre Home Prices Going To Fall?

-

Affordability4 weeks ago

Affordability4 weeks agoNewly Built Home Prices Hit a 5-Year Low

-

Affordability3 weeks ago

Affordability3 weeks agoWhat Most Veterans Don’t Know About Their VA Home Loan Benefit

-

Affordability3 weeks ago

Affordability3 weeks agoThe Truth About Affordability Today

-

For Sellers3 weeks ago

For Sellers3 weeks agoThe Real Reason Some People Are Still Moving Right Now

-

Economy2 weeks ago

Economy2 weeks agoThe Mid-Year Housing Market Update: Why Forecasts Changed in 2026

-

Affordability2 weeks ago

Affordability2 weeks agoWhat Rising Inflation Means for Your Move

You must be logged in to post a comment Login